3 |

3 |

2 |

3 |

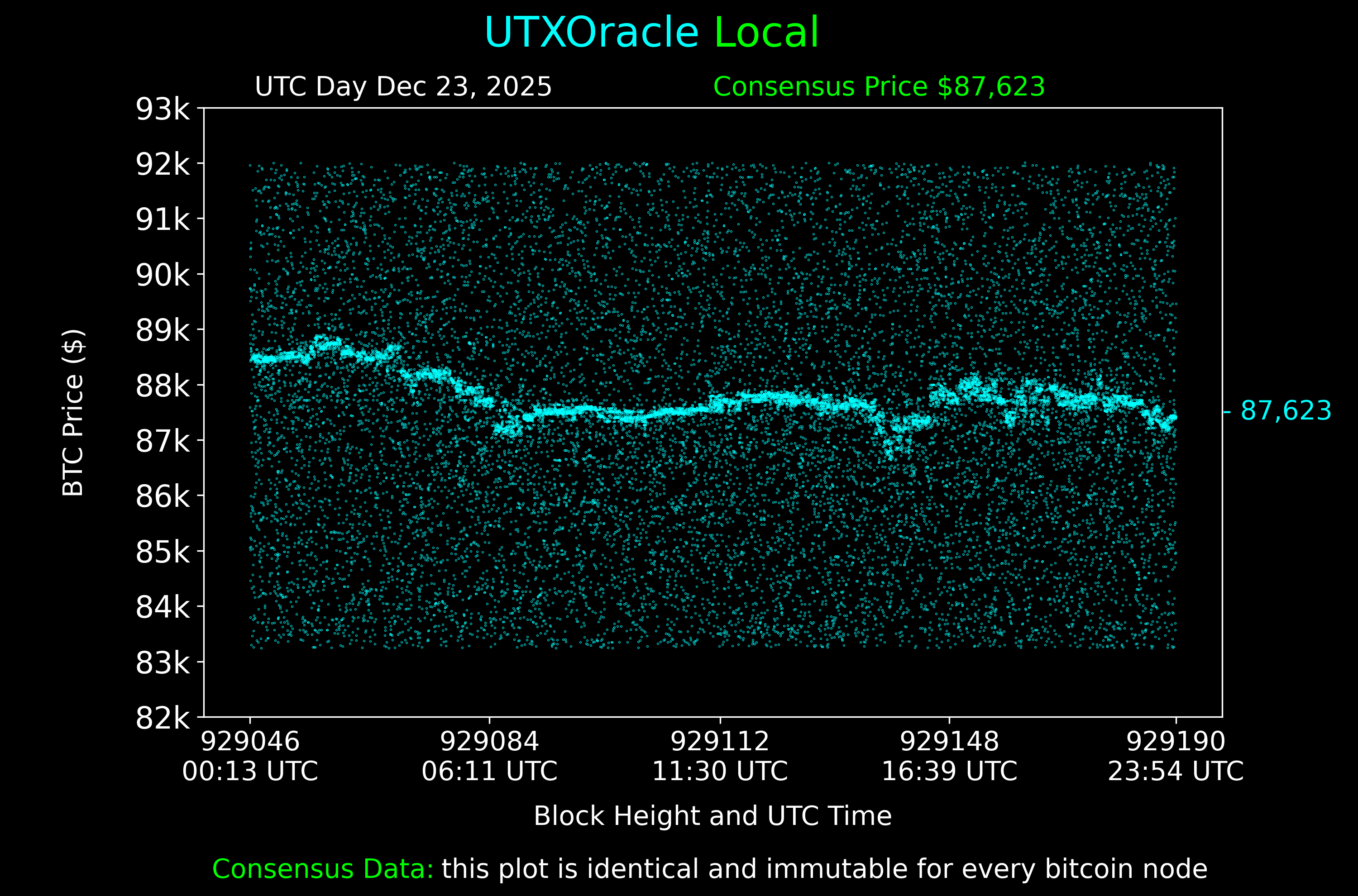

87 | Signal from noise. 88 |