├── btc_mp_v1.bat

├── btc_mp_v1.sh

├── LICENSE

├── README.md

├── btc_mp_v1.py

└── MP.py

/btc_mp_v1.bat:

--------------------------------------------------------------------------------

1 | start "" http://127.0.0.1:8000/ & python.exe C:\anaconda\Scripts\dash_2\BTC_mp_v2.py

2 |

--------------------------------------------------------------------------------

/btc_mp_v1.sh:

--------------------------------------------------------------------------------

1 | #!/bin/sh

2 | xdg-open http://127.0.0.1:8000/ & python3.8 /home/alex2/scripts/dash_2/btc_mp_v1.py

3 |

--------------------------------------------------------------------------------

/LICENSE:

--------------------------------------------------------------------------------

1 | MIT License

2 |

3 | Copyright (c) 2021 beinghorizontal

4 |

5 | Permission is hereby granted, free of charge, to any person obtaining a copy

6 | of this software and associated documentation files (the "Software"), to deal

7 | in the Software without restriction, including without limitation the rights

8 | to use, copy, modify, merge, publish, distribute, sublicense, and/or sell

9 | copies of the Software, and to permit persons to whom the Software is

10 | furnished to do so, subject to the following conditions:

11 |

12 | The above copyright notice and this permission notice shall be included in all

13 | copies or substantial portions of the Software.

14 |

15 | THE SOFTWARE IS PROVIDED "AS IS", WITHOUT WARRANTY OF ANY KIND, EXPRESS OR

16 | IMPLIED, INCLUDING BUT NOT LIMITED TO THE WARRANTIES OF MERCHANTABILITY,

17 | FITNESS FOR A PARTICULAR PURPOSE AND NONINFRINGEMENT. IN NO EVENT SHALL THE

18 | AUTHORS OR COPYRIGHT HOLDERS BE LIABLE FOR ANY CLAIM, DAMAGES OR OTHER

19 | LIABILITY, WHETHER IN AN ACTION OF CONTRACT, TORT OR OTHERWISE, ARISING FROM,

20 | OUT OF OR IN CONNECTION WITH THE SOFTWARE OR THE USE OR OTHER DEALINGS IN THE

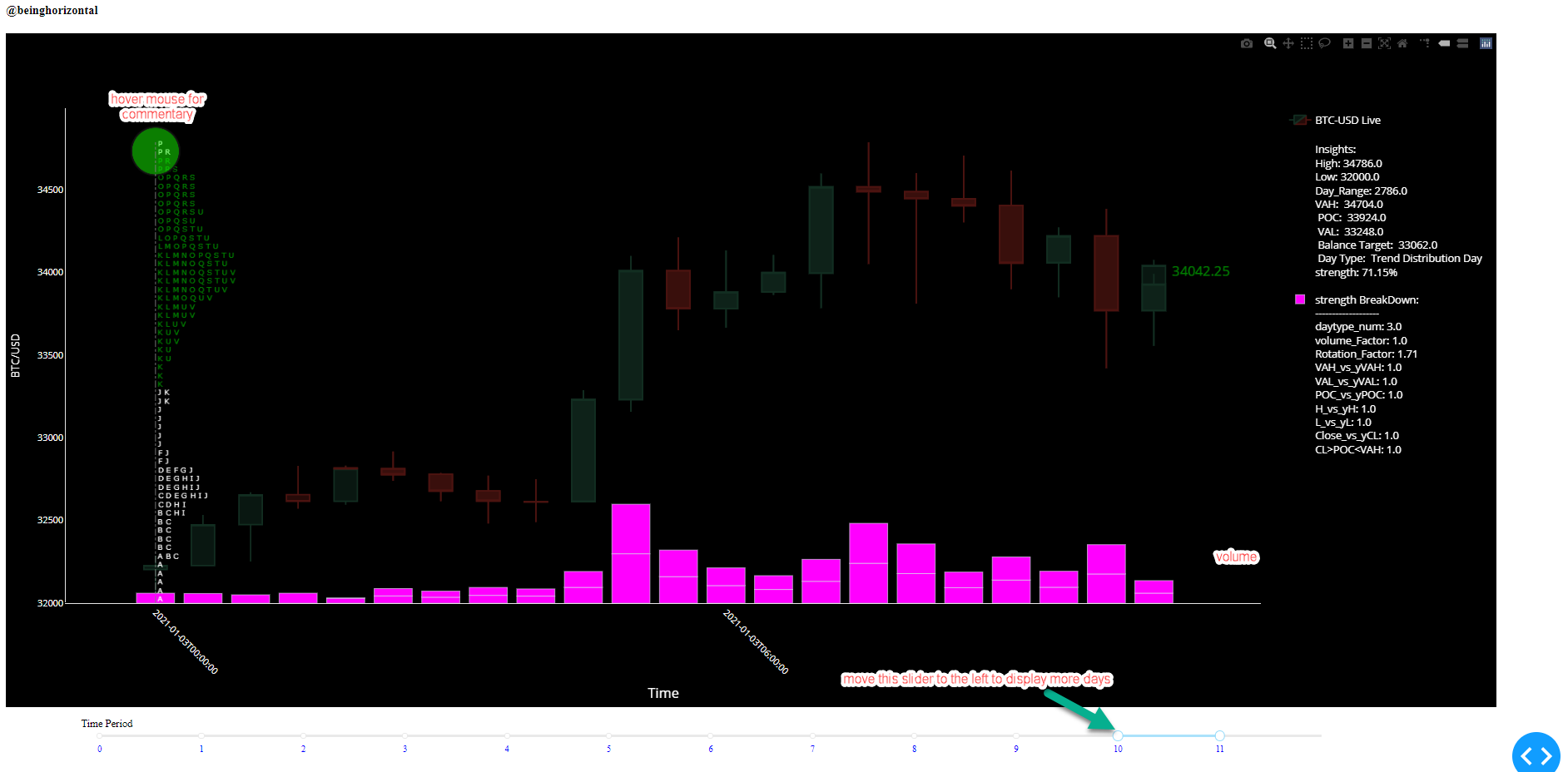

21 | SOFTWARE.

22 |

--------------------------------------------------------------------------------

/README.md:

--------------------------------------------------------------------------------

1 | # tpo_btc

2 | This is a Python visualization code. It fetches BTC data from Binance servers and streams live market profile chart using Dash. This code is the modification of my existing old code posted here https://github.com/beinghorizontal/tpo_project/

3 |

4 | ## Dependencies

5 | pip install plotly (update if previously installed)

6 |

7 | pip install dash (update if previously installed)

8 |

9 | pip install pandas

10 |

11 | pip install requests

12 |

13 | ## Steps for live chat

14 |

15 | Download all the files or clone this repo as a zip and extract it in a local folder.

16 |

17 | In Windows: a) Edit btc_mp_v2.bat file (right-click, open in notepad) and change the URL where you saved btc_mp_v2.py and save it

18 | eg. start "" http://127.0.0.1:8000/ & python.exe C:\here_i_saved_the_file\btc_mp_v2.py

19 | b) Double click the .bat file and a new tab will open in your default browser, wait for few seconds as it takes time to fetch the data from the servers and finish the one-time calculations for the context (this delay is only when you first run the batch script) and live chat will get automatically updated. That's it.

20 |

21 | In Linux: a) Edit btc_mp_v2.sh and change the URL where you saved btc_mp_v2.py and save it.

22 | b) You have to make this shell script executable. Open the command prompt, cd to where you saved the python file and type chmod +x btc_mp_v2.py

23 | c) Double click the .sh file and a new tab will open in your default browser, wait for few seconds as it takes time to fetch the data from the servers and finish the one-time calculations for the context (this delay is only when you first run the shell script) and live chat will get automatically updated. That's it.

24 |

25 | By default only the current day is displayed, if you want to see more than one day then adjust the slider at the bottom (see the 1st image below)

26 |

27 | If you want to use volume profile instead of TPO profile (based on price), then edit the code btc_mp_v1.py and go to the line 55 and replace mode ='tpo' by mode ='vol'. You don't need to close the live chart if it is open, chart will automatically refresh (Unless you executed the code from ipython console) and the code will use volume for all market profile related calculations.

28 |

29 | ## What is new

30 |

31 | The old code was for the local data while this one fetches the live data for BTC-USD directly from Binance servers in 30 minute format for last 10 days (binance limitation) You can use it for any other pair supported by Binance. Fetching the data part is actually very small. Any URL that supports 30-minute data with a minimum history of 10 days will work with this code.

32 |

33 | Wrote one big class for all market profile and day ranking related calculations instead of functions which is the heart of the code. It also means no repeat calculations and more readable code

34 |

35 | Added volume bars at the bottom

36 |

37 | Removed Initial Balance (Opening range) related calculations as it was impacting the stability of the code and also it doesn't make sense to use the initial balance for 24-hour scrips like bitcoin-USD pair or any other Forex pair.

38 |

39 | Insights and strength breakdown for the current day are displayed to the right and will get updated live. You can also hover the mouse over circles on top of market profile chart to see the insights (Those who are new to the plotly ecosystem, hover text is supported by plotly by default and Dash is the extension of Plotly).

40 |

41 | Factors that are not contributing to the strength (where value = 0 in breakdown part) will get dynamically omitted to reduce the clutter and increase the readability. Also, when these factors are in play they will get automatically added in breakdown commentary (where breakdown value != 0).

42 |

43 | ## This is how the chart looks like in the new version

44 |

45 |

46 |

47 | ## General overview of the TPO chart produced by the algo (ignore the price as I copied this from readme section of the old versionThe)

48 |

49 |

50 |

51 | ## Bubbles at the top:

52 |

53 |

54 | # Disclaimer about balanced target

55 | if you read the insights and it's breakdown carefully there is a one line called a balanced target. So what is it and how important it is? well, I don't believe in using market profile as an indicator but thought to add this line as it indicates where the mean reversion target will be. This will be highly dangerous to use in scrips like Bitcoin or in general when the market is in strong trend.

56 |

57 | In the simplest form this is how it works. If there is an imbalance between POC -VAL and VAH-POC ( when price excessively moves to one direction) then it assumes that price will revert back and then it updates the balanced target. Don't take it too seriously, back then it used to work well in E-mini.

58 |

59 | # Final thoughts

60 |

61 | If you don't know anything about Market Profile (TM) then you might not understand the whole concept completely. If you're interested then do read the small handbook on Auction Market Theory(direct link below). Don't get confused by the name, AMT and Market Profile is the same thing. In short, the concept is based on how Auctions work. Of course the concept is not as deep as that 2020 Nobel Prize winner in Economics and quite frankly this one is quite usable. Usable in the sense most of the part is quantifiable. At the end of day it is a visual tool to assist the decision process and not an execution tool. In other words market profile is not an indicator or any kind of signal.

62 | # Link

63 | CBOT Market Profile handbook (13 mb pdf) https://t.co/L8DfNkLNi5?amp=1

64 |

--------------------------------------------------------------------------------

/btc_mp_v1.py:

--------------------------------------------------------------------------------

1 | from MP import MpFunctions

2 | import requests

3 | import dash

4 | import dash_core_components as dcc

5 | import dash_html_components as html

6 | from dash.dependencies import Input, Output

7 | import pandas as pd

8 | import plotly.graph_objs as go

9 | import datetime as dt

10 | import numpy as np

11 | import warnings

12 |

13 | warnings.filterwarnings('ignore')

14 |

15 | app = dash.Dash(__name__)

16 |

17 | def get_ticksize(data, freq=30):

18 | # data = dflive30

19 | numlen = int(len(data) / 2)

20 | # sample size for calculating ticksize = 50% of most recent data

21 | tztail = data.tail(numlen).copy()

22 | tztail['tz'] = tztail.Close.rolling(freq).std() # std. dev of 30 period rolling

23 | tztail = tztail.dropna()

24 | ticksize = np.ceil(tztail['tz'].mean() * 0.25) # 1/4 th of mean std. dev is our ticksize

25 |

26 | if ticksize < 0.2:

27 | ticksize = 0.2 # minimum ticksize limit

28 |

29 | return int(ticksize)

30 |

31 | def get_data(url):

32 | """

33 | :param url: binance url

34 | :return: ohlcv dataframe

35 | """

36 | response = requests.get(url)

37 | data = response.json()

38 | df = pd.DataFrame(data)

39 | df = df.apply(pd.to_numeric)

40 | df[0] = pd.to_datetime(df[0], unit='ms')

41 | df = df[[0, 1, 2, 3, 4, 5]]

42 | df.columns = ['datetime', 'Open', 'High', 'Low', 'Close', 'volume']

43 | df = df.set_index('datetime', inplace=False, drop=False)

44 | return df

45 |

46 |

47 | url_30m = "https://www.binance.com/api/v1/klines?symbol=BTCBUSD&interval=30m" # 10 days history 30 min ohlcv

48 | df = get_data(url_30m)

49 | df.to_csv('btcusd30m.csv', index=False)

50 |

51 | # params

52 | context_days = len([group[1] for group in df.groupby(df.index.date)]) # Number of days used for context

53 | freq = 2 # for 1 min bar use 30 min frequency for each TPO, here we fetch default 30 min bars server

54 | avglen = context_days - 2 # num days to calculate average values

55 | mode = 'tpo' # for volume --> 'vol'

56 | trading_hr = 24 # Default for BTC USD or Forex

57 | day_back = 0 # -1 While testing sometimes maybe you don't want current days data then use -1

58 | # ticksz = 28 # If you want to use manual tick size then uncomment this. Really small number means convoluted alphabets (TPO)

59 | ticksz = (get_ticksize(df.copy(), freq=freq))*2 # Algorithm will calculate the optimal tick size based on volatility

60 | textsize = 10

61 |

62 | if day_back != 0:

63 | symbol = 'Historical Mode'

64 | else:

65 | symbol = 'BTC-USD Live'

66 |

67 | dfnflist = [group[1] for group in df.groupby(df.index.date)] #

68 |

69 | dates = []

70 | for d in range(0, len(dfnflist)):

71 | dates.append(dfnflist[d].index[0])

72 |

73 | date_time_close = dt.datetime.today().strftime('%Y-%m-%d') + ' ' + '23:59:59'

74 | append_dt = pd.Timestamp(date_time_close)

75 | dates.append(append_dt)

76 | date_mark = {str(h): {'label': str(h), 'style': {'color': 'blue', 'fontsize': '4',

77 | 'text-orientation': 'upright'}} for h in range(0, len(dates))}

78 |

79 | mp = MpFunctions(data=df.copy(), freq=freq, style=mode, avglen=avglen, ticksize=ticksz, session_hr=trading_hr)

80 | mplist = mp.get_context()

81 |

82 | app.layout = html.Div(

83 | html.Div([

84 | dcc.Location(id='url', refresh=False),

85 | dcc.Link('Twitter', href='https://twitter.com/beinghorizontal'),

86 | html.Br(),

87 | dcc.Link('python source code', href='http://www.github.com/beinghorizontal'),

88 | html.H4('@beinghorizontal'),

89 | dcc.Graph(id='beinghorizontal'),

90 | dcc.Interval(

91 | id='interval-component',

92 | interval=5 * 1000, # Reduce the time if you want frequent updates 5000 = 5 sec

93 | n_intervals=0

94 | ),

95 | html.P([

96 | html.Label("Time Period"),

97 | dcc.RangeSlider(id='slider',

98 | pushable=1,

99 | marks=date_mark,

100 | min=0,

101 | max=len(dates),

102 | step=None,

103 | value=[len(dates) - 2, len(dates) - 1])

104 | ], style={'width': '80%',

105 | 'fontSize': '14px',

106 | 'padding-left': '100px',

107 | 'display': 'inline-block'})

108 | ])

109 | )

110 |

111 |

112 | @app.callback(Output(component_id='beinghorizontal', component_property='figure'),

113 | [Input('interval-component', 'n_intervals'),

114 | Input('slider', 'value')

115 | ])

116 | def update_graph(n, value):

117 | listmp_hist = mplist[0]

118 | distribution_hist = mplist[1]

119 |

120 | url_1m = "https://www.binance.com/api/v1/klines?symbol=BTCBUSD&interval=1m"

121 |

122 | df_live1 = get_data(url_1m) # this line fetches new data for current day

123 | df_live1 = df_live1.dropna()

124 |

125 | dflive30 = df_live1.resample('30min').agg({'datetime': 'last', 'Open': 'first', 'High': 'max', 'Low': 'min',

126 | 'Close': 'last', 'volume': 'sum'})

127 | df2 = pd.concat([df, dflive30])

128 | df2 = df2.drop_duplicates('datetime')

129 |

130 | ticksz_live = (get_ticksize(dflive30.copy(), freq=2))

131 | mplive = MpFunctions(data=dflive30.copy(), freq=freq, style=mode, avglen=avglen, ticksize=ticksz_live,

132 | session_hr=trading_hr)

133 | mplist_live = mplive.get_context()

134 | listmp_live = mplist_live[0] # it will be in list format so take [0] slice for current day MP data frame

135 | df_distribution_live = mplist_live[1]

136 | df_distribution_concat = pd.concat([distribution_hist, df_distribution_live], axis=0)

137 | df_distribution_concat = df_distribution_concat.reset_index(inplace=False, drop=True)

138 |

139 | df_updated_rank = mp.get_dayrank()

140 | ranking = df_updated_rank[0]

141 | power1 = ranking.power1 # Non-normalised IB strength

142 | power = ranking.power # Normalised IB strength for dynamic shape size for markers at bottom

143 | breakdown = df_updated_rank[1]

144 | dh_list = ranking.highd

145 | dl_list = ranking.lowd

146 |

147 | listmp = listmp_hist + listmp_live

148 |

149 | df3 = df2[(df2.index >= dates[value[0]]) & (df2.index <= dates[value[1]])]

150 | DFList = [group[1] for group in df2.groupby(df2.index.date)]

151 |

152 | fig = go.Figure(data=[go.Candlestick(x=df3.index,

153 |

154 | open=df3['Open'],

155 | high=df3['High'],

156 | low=df3['Low'],

157 | close=df3['Close'],

158 | showlegend=True,

159 | name=symbol,

160 | opacity=0.3)]) # To make candlesticks more prominent increase the opacity

161 |

162 | for inc in range(value[1] - value[0]):

163 | i = value[0]

164 | # inc = 0 # for debug

165 | # i = value[0]

166 |

167 | i += inc

168 | df1 = DFList[i].copy()

169 | df_mp = listmp[i]

170 | irank = ranking.iloc[i] # select single row from ranking df

171 | df_mp['i_date'] = df1['datetime'][0]

172 | # # @todo: background color for text

173 | df_mp['color'] = np.where(np.logical_and(

174 | df_mp['close'] > irank.vallist, df_mp['close'] < irank.vahlist), 'green', 'white')

175 |

176 | df_mp = df_mp.set_index('i_date', inplace=False)

177 |

178 | # print(df_mp.index)

179 | fig.add_trace(

180 | go.Scattergl(x=df_mp.index, y=df_mp.close, mode="text", text=df_mp.alphabets,

181 | showlegend=False, textposition="top right",

182 | textfont=dict(family="verdana", size=textsize, color=df_mp.color)))

183 |

184 | if power1[i] < 0:

185 | my_rgb = 'rgba({power}, 3, 252, 0.5)'.format(power=abs(165))

186 | else:

187 | my_rgb = 'rgba(23, {power}, 3, 0.5)'.format(power=abs(252))

188 |

189 | brk_f_list_maj = []

190 | f = 0

191 | for f in range(len(breakdown.columns)):

192 | brk_f_list_min = []

193 | for index, rows in breakdown.iterrows():

194 | if rows[f] != 0:

195 | brk_f_list_min.append(index + str(': ') + str(rows[f]) + '

')

196 | brk_f_list_maj.append(brk_f_list_min)

197 |

198 | breakdown_values = '' # for bubble callouts

199 | for st in brk_f_list_maj[i]:

200 | breakdown_values += st

201 | commentary_text = (

202 | '

Insights:

High: {}

Low: {}

Day_Range: {}

VAH: {}

POC: {}

VAL: {}

Balance Target: '

203 | '{}

Day Type: {}

strength: {}%

strength BreakDown: {}

{}

{}'.format(

204 | dh_list[i], dl_list[i],round(dh_list[i]- dl_list[i],2),

205 | irank.vahlist,

206 | irank.poclist, irank.vallist, irank.btlist, irank.daytype, irank.power, '',

207 | '-------------------', breakdown_values))

208 |

209 |

210 | fig.add_trace(go.Scattergl(

211 | x=[irank.date],

212 | y=[df3['High'].max() - (ticksz)],

213 | mode="markers",

214 | marker=dict(color=my_rgb, size=0.90 * power[i],

215 | line=dict(color='rgb(17, 17, 17)', width=2)),

216 | # marker_symbol='square',

217 | hovertext=commentary_text, showlegend=False))

218 |

219 | lvns = irank.lvnlist

220 |

221 | for lvn in lvns:

222 | if lvn > irank.vallist and lvn < irank.vahlist:

223 | fig.add_shape(

224 | # Line Horizontal

225 | type="line",

226 | x0=df_mp.index[0],

227 | y0=lvn,

228 | x1=df_mp.index[0] + dt.timedelta(hours=1),

229 | y1=lvn,

230 | line=dict(

231 | color="darksalmon",

232 | width=2,

233 | dash="dashdot", ), )

234 |

235 | fig.add_shape(

236 | type="line",

237 | x0=df_mp.index[0],

238 | y0=dl_list[i],

239 | x1=df_mp.index[0],

240 | y1=dh_list[i],

241 | line=dict(

242 | color="gray",

243 | width=1,

244 | dash="dashdot", ), )

245 |

246 | fig.layout.xaxis.type = 'category' # This line will omit annoying weekends on the plotly graph

247 |

248 | ltp = df1.iloc[-1]['Close']

249 | if ltp >= irank.poclist:

250 | ltp_color = 'green'

251 | else:

252 | ltp_color = 'red'

253 |

254 | fig.add_trace(go.Bar(x=df3.index, y=df3['volume'], marker=dict(color='magenta'), yaxis='y3', name=str(commentary_text)))

255 |

256 | fig.add_trace(go.Scattergl(

257 | x=[df3.iloc[-1]['datetime']],

258 | y=[df3.iloc[-1]['Close']],

259 | mode="text",

260 | name="last traded price",

261 | text=[str(df3.iloc[-1]['Close'])],

262 | textposition="bottom center",

263 | textfont=dict(size=18, color=ltp_color),

264 | showlegend=False

265 | ))

266 | # to make x-axis less crowded

267 | if value[1] - value[0] > 4:

268 | dticksv = 30

269 | else:

270 | dticksv = len(dates)

271 | y3min = df3['volume'].min()

272 | y3max = df3['volume'].max() * 10

273 | ymin = df3['Low'].min()

274 | ymax = df3['High'].max() + (4 * ticksz)

275 |

276 | # Adjust height & width according to your monitor size & orientation.

277 | fig.update_layout(paper_bgcolor='black', plot_bgcolor='black', height=900, width=1990,

278 | xaxis=dict(showline=True, color='white', type='category', title_text='Time', tickangle=45,

279 | dtick=dticksv, title_font=dict(size=18, color='white')),

280 | yaxis=dict(showline=True, color='white', range=[ymin, ymax], showgrid=False,

281 | title_text='BTC/USD'),

282 | yaxis2=dict(showgrid=False),

283 | yaxis3=dict(range=[y3min, y3max], overlaying="y",

284 | side="right",

285 | color='black',

286 | showgrid=False),

287 | legend=dict(font=dict(color='White',size=14)))

288 |

289 | fig.update_layout(yaxis_tickformat='d')

290 | fig["layout"]["xaxis"]["rangeslider"]["visible"] = False

291 | fig["layout"]["xaxis"]["tickformat"] = "%H:%M:%S"

292 |

293 | # plot(fig, auto_open=True) # For debugging

294 | return (fig)

295 |

296 |

297 | if __name__ == '__main__':

298 | app.run_server(port=8000, host='127.0.0.1',

299 | debug=True) # debug=False if executing from ipython(vscode/Pycharm/Spyder)

300 |

--------------------------------------------------------------------------------

/MP.py:

--------------------------------------------------------------------------------

1 | # -*- coding: utf-8 -*-

2 | """

3 | Created on Mon Jul 27 13:26:04 2020

4 |

5 | @author: alex1

6 | """

7 | import math

8 | import numpy as np

9 | import pandas as pd

10 |

11 |

12 | # # debug

13 | # mp = MpFunctions(data=df, freq=2, style='tpo', avglen=8, ticksize=24, session_hr=24)

14 | # mplist = mp.get_context()

15 | # #mplist[1]

16 | # meandict = mp.get_mean()

17 | # #meandict['volume_mean']

18 |

19 |

20 | class MpFunctions():

21 | def __init__(self, data, freq=30, style='tpo', avglen=8, ticksize=8, session_hr=8):

22 | self.data = data

23 | self.freq = freq

24 | self.style = style

25 | self.avglen = avglen

26 | self.ticksize = ticksize

27 | self.session_hr = session_hr

28 |

29 | def get_ticksize(self):

30 | # data = df

31 | numlen = int(len(self.data) / 2)

32 | # sample size for calculating ticksize = 50% of most recent data

33 | tztail = self.data.tail(numlen).copy()

34 | tztail['tz'] = tztail.Close.rolling(self.freq).std() # std. dev of 30 period rolling

35 | tztail = tztail.dropna()

36 | ticksize = np.ceil(tztail['tz'].mean() * 0.25) # 1/4 th of mean std. dev is our ticksize

37 |

38 | if ticksize < 0.2:

39 | ticksize = 0.2 # minimum ticksize limit

40 |

41 | return int(ticksize)

42 |

43 | def abc(self):

44 | caps = [' A', ' B', ' C', ' D', ' E', ' F', ' G', ' H', ' I', ' J', ' K', ' L', ' M',

45 | ' N', ' O', ' P', ' Q', ' R', ' S', ' T', ' U', ' V', ' W', ' X', ' Y', ' Z']

46 | abc_lw = [x.lower() for x in caps]

47 | Aa = caps + abc_lw

48 | alimit = math.ceil(self.session_hr * (60 / self.freq)) + 3

49 | if alimit > 52:

50 | alphabets = Aa * int(

51 | (np.ceil((alimit - 52) / 52)) + 1) # if bar frequency is less than 30 minutes then multiply list

52 | else:

53 | alphabets = Aa[0:alimit]

54 | bk = [28, 31, 35, 40, 33, 34, 41, 44, 35, 52, 41, 40, 46, 27, 38]

55 | ti = []

56 | for s1 in bk:

57 | ti.append(Aa[s1 - 1])

58 | tt = (''.join(ti))

59 |

60 | return alphabets, tt

61 |

62 | def get_rf(self):

63 | self.data['cup'] = np.where(self.data['Close'] >= self.data['Close'].shift(), 1, -1)

64 | self.data['hup'] = np.where(self.data['High'] >= self.data['High'].shift(), 1, -1)

65 | self.data['lup'] = np.where(self.data['Low'] >= self.data['Low'].shift(), 1, -1)

66 |

67 | self.data['rf'] = self.data['cup'] + self.data['hup'] + self.data['lup']

68 | dataf = self.data.drop(['cup', 'lup', 'hup'], axis=1)

69 | return dataf

70 |

71 | def get_mean(self):

72 | """

73 | dfhist: pandas dataframe 1 min frequency

74 | avglen: Length for mean values

75 | freq: timeframe for the candlestick & TPOs

76 |

77 | return: a) daily mean for volume, rotational factor (absolute value), IB volume, IB RF b) session length

78 | dfhist = df.copy()

79 | """

80 | dfhist = self.get_rf()

81 | # dfhist = get_rf(dfhist.copy())

82 | dfhistd = dfhist.resample("D").agg(

83 | {'Open': 'first', 'High': 'max', 'Low': 'min', 'Close': 'last', 'volume': 'sum',

84 | 'rf': 'sum', })

85 | dfhistd = dfhistd.dropna()

86 | comp_days = len(dfhistd)

87 |

88 | vm30 = dfhistd['volume'].rolling(self.avglen).mean()

89 | volume_mean = vm30[len(vm30) - 1]

90 | rf30 = abs((dfhistd['rf'])).rolling(

91 | self.avglen).mean() # it is abs mean to get meaningful value to compare daily values

92 | rf_mean = rf30[len(rf30) - 1]

93 |

94 | date2 = dfhistd.index[1].date()

95 | mask = dfhist.index.date < date2

96 | dfsession = dfhist.loc[mask]

97 | session_hr = math.ceil(len(dfsession) / 60)

98 |

99 | all_val = dict(volume_mean=volume_mean, rf_mean=rf_mean, session_hr=session_hr)

100 |

101 | return all_val

102 |

103 | def tpo(self, dft_rs):

104 | # dft_rs = dfc1.copy()

105 | # if len(dft_rs) > int(60 / freq):

106 | if len(dft_rs) > int(0):

107 | dft_rs = dft_rs.drop_duplicates('datetime')

108 | dft_rs = dft_rs.reset_index(inplace=False, drop=True)

109 | dft_rs['rol_mx'] = dft_rs['High'].cummax()

110 | dft_rs['rol_mn'] = dft_rs['Low'].cummin()

111 | dft_rs['ext_up'] = dft_rs['rol_mn'] > dft_rs['rol_mx'].shift(2)

112 | dft_rs['ext_dn'] = dft_rs['rol_mx'] < dft_rs['rol_mn'].shift(2)

113 | alphabets = self.abc()[0]

114 | # alphabets = abc(session_hr, freq)[0]

115 | alphabets = alphabets[0:len(dft_rs)]

116 | hh = dft_rs['High'].max()

117 | ll = dft_rs['Low'].min()

118 | day_range = hh - ll

119 | dft_rs['abc'] = alphabets

120 | # place represents total number of steps to take to compare the TPO count

121 | place = int(np.ceil((hh - ll) / self.ticksize))

122 | # kk = 0

123 | abl_bg = []

124 | tpo_countbg = []

125 | pricel = []

126 | volcountbg = []

127 | # datel = []

128 | for u in range(place):

129 | abl = []

130 | tpoc = []

131 | volcount = []

132 | p = ll + (u * self.ticksize)

133 | for lenrs in range(len(dft_rs)):

134 | if p >= dft_rs['Low'][lenrs] and p < dft_rs['High'][lenrs]:

135 | abl.append(dft_rs['abc'][lenrs])

136 | tpoc.append(1)

137 | volcount.append((dft_rs['volume'][lenrs]) / self.freq)

138 | abl_bg.append(''.join(abl))

139 | tpo_countbg.append(sum(tpoc))

140 | volcountbg.append(sum(volcount))

141 | pricel.append(p)

142 |

143 | dftpo = pd.DataFrame({'close': pricel, 'alphabets': abl_bg,

144 | 'tpocount': tpo_countbg, 'volsum': volcountbg})

145 | # drop empty rows

146 | dftpo['alphabets'].replace('', np.nan, inplace=True)

147 | dftpo = dftpo.dropna()

148 | dftpo = dftpo.reset_index(inplace=False, drop=True)

149 | dftpo = dftpo.sort_index(ascending=False)

150 | dftpo = dftpo.reset_index(inplace=False, drop=True)

151 |

152 | if self.style == 'tpo':

153 | column = 'tpocount'

154 | else:

155 | column = 'volsum'

156 |

157 | dfmx = dftpo[dftpo[column] == dftpo[column].max()]

158 |

159 | mid = ll + ((hh - ll) / 2)

160 | dfmax = dfmx.copy()

161 | dfmax['poc-mid'] = abs(dfmax['close'] - mid)

162 | pocidx = dfmax['poc-mid'].idxmin()

163 | poc = dfmax['close'][pocidx]

164 | poctpo = dftpo[column].max()

165 | tpo_updf = dftpo[dftpo['close'] > poc]

166 | tpo_updf = tpo_updf.sort_index(ascending=False)

167 | tpo_updf = tpo_updf.reset_index(inplace=False, drop=True)

168 |

169 | tpo_dndf = dftpo[dftpo['close'] < poc]

170 | tpo_dndf = tpo_dndf.reset_index(inplace=False, drop=True)

171 |

172 | valtpo = (dftpo[column].sum()) * 0.70

173 |

174 | abovepoc = tpo_updf[column].to_list()

175 | belowpoc = tpo_dndf[column].to_list()

176 |

177 | if (len(abovepoc) / 2).is_integer() is False:

178 | abovepoc = abovepoc + [0]

179 |

180 | if (len(belowpoc) / 2).is_integer() is False:

181 | belowpoc = belowpoc + [0]

182 |

183 | bel2 = np.array(belowpoc).reshape(-1, 2)

184 | bel3 = bel2.sum(axis=1)

185 | bel4 = list(bel3)

186 | abv2 = np.array(abovepoc).reshape(-1, 2)

187 | abv3 = abv2.sum(axis=1)

188 | abv4 = list(abv3)

189 | # cum = poctpo

190 | # up_i = 0

191 | # dn_i = 0

192 | df_va = pd.DataFrame({'abv': pd.Series(abv4), 'bel': pd.Series(bel4)})

193 | df_va = df_va.fillna(0)

194 | df_va['abv_idx'] = np.where(df_va.abv > df_va.bel, 1, 0)

195 | df_va['bel_idx'] = np.where(df_va.bel > df_va.abv, 1, 0)

196 | df_va['cum_tpo'] = np.where(df_va.abv > df_va.bel, df_va.abv, 0)

197 | df_va['cum_tpo'] = np.where(df_va.bel > df_va.abv, df_va.bel, df_va.cum_tpo)

198 |

199 | df_va['cum_tpo'] = np.where(df_va.abv == df_va.bel, df_va.abv + df_va.bel, df_va.cum_tpo)

200 | df_va['abv_idx'] = np.where(df_va.abv == df_va.bel, 1, df_va.abv_idx)

201 | df_va['bel_idx'] = np.where(df_va.abv == df_va.bel, 1, df_va.bel_idx)

202 | df_va['cum_tpo_cumsum'] = df_va.cum_tpo.cumsum()

203 | # haven't add poc tpo because loop cuts off way before 70% so it gives same effect

204 | df_va_cut = df_va[df_va.cum_tpo_cumsum + poctpo <= valtpo]

205 | vah_idx = (df_va_cut.abv_idx.sum()) * 2

206 | val_idx = (df_va_cut.bel_idx.sum()) * 2

207 |

208 | if vah_idx >= len(tpo_updf) and vah_idx != 0:

209 | vah_idx = vah_idx - 2

210 |

211 | if val_idx >= len(tpo_dndf) and val_idx != 0:

212 | val_idx = val_idx - 2

213 |

214 | vah = tpo_updf.close[vah_idx]

215 | val = tpo_dndf.close[val_idx]

216 |

217 | tpoval = dftpo[self.ticksize:-(self.ticksize)]['tpocount'] # take mid section

218 | exhandle_index = np.where(tpoval <= 2, tpoval.index, None) # get index where TPOs are 2

219 | exhandle_index = list(filter(None, exhandle_index))

220 | distance = self.ticksize * 3 # distance b/w two ex handles / lvn

221 | lvn_list = []

222 | for ex in exhandle_index[0:-1:distance]:

223 | lvn_list.append(dftpo['close'][ex])

224 |

225 | area_above_poc = dft_rs.High.max() - poc

226 | area_below_poc = poc - dft_rs.Low.min()

227 | if area_above_poc == 0:

228 | area_above_poc = 1

229 | if area_below_poc == 0:

230 | area_below_poc = 1

231 | balance = area_above_poc / area_below_poc

232 |

233 | if balance >= 0:

234 | bal_target = poc - area_above_poc

235 | else:

236 | bal_target = poc + area_below_poc

237 |

238 | mp = {'df': dftpo, 'vah': round(vah, 2), 'poc': round(poc, 2), 'val': round(val, 2), 'lvn': lvn_list,

239 | 'bal_target': round(bal_target, 2)}

240 |

241 | else:

242 | print('not enough bars for date {}'.format(dft_rs['datetime'][0]))

243 | mp = {}

244 |

245 | return mp

246 |

247 | # !!! fetch all MP derived results here with date and do extra context analysis

248 |

249 | def get_context(self):

250 | df_hi = self.get_rf()

251 | try:

252 | # df_hi = dflive30.copy() # testing

253 | DFcontext = [group[1] for group in df_hi.groupby(df_hi.index.date)]

254 | dfmp_l = []

255 | i_poctpo_l = []

256 | i_tposum = []

257 | vah_l = []

258 | poc_l = []

259 | val_l = []

260 | bt_l = []

261 | lvn_l = []

262 | # excess_l = []

263 | date_l = []

264 | volume_l = []

265 | rf_l = []

266 | # ibv_l = []

267 | # ibrf_l = []

268 | # ibh_l = []

269 | # ib_l = []

270 | close_l = []

271 | hh_l = []

272 | ll_l = []

273 | range_l = []

274 |

275 | for c in range(len(DFcontext)): # c=0 for testing

276 | dfc1 = DFcontext[c].copy()

277 | # dfc1.iloc[:, 2:6] = dfc1.iloc[:, 2:6].apply(pd.to_numeric)

278 |

279 | dfc1 = dfc1.reset_index(inplace=False, drop=True)

280 | mpc = self.tpo(dfc1)

281 | dftmp = mpc['df']

282 | dfmp_l.append(dftmp)

283 | # for day types

284 | i_poctpo_l.append(dftmp['tpocount'].max())

285 | i_tposum.append(dftmp['tpocount'].sum())

286 | # !!! get value areas

287 | vah_l.append(mpc['vah'])

288 | poc_l.append(mpc['poc'])

289 | val_l.append(mpc['val'])

290 |

291 | bt_l.append(mpc['bal_target'])

292 | lvn_l.append(mpc['lvn'])

293 | # excess_l.append(mpc['excess'])

294 |

295 | # !!! operatio of non profile stats

296 | date_l.append(dfc1.datetime[0])

297 | close_l.append(dfc1.iloc[-1]['Close'])

298 | hh_l.append(dfc1.High.max())

299 | ll_l.append(dfc1.Low.min())

300 | range_l.append(dfc1.High.max() - dfc1.Low.min())

301 |

302 | volume_l.append(dfc1.volume.sum())

303 | rf_l.append(dfc1.rf.sum())

304 | # !!! get IB

305 | dfc1['cumsumvol'] = dfc1.volume.cumsum()

306 | dfc1['cumsumrf'] = dfc1.rf.cumsum()

307 | dfc1['cumsumhigh'] = dfc1.High.cummax()

308 | dfc1['cumsummin'] = dfc1.Low.cummin()

309 |

310 | dist_df = pd.DataFrame({'date': date_l, 'maxtpo': i_poctpo_l, 'tpocount': i_tposum, 'vahlist': vah_l,

311 | 'poclist': poc_l, 'vallist': val_l, 'btlist': bt_l, 'lvnlist': lvn_l,

312 | 'volumed': volume_l, 'rfd': rf_l, 'highd': hh_l, 'lowd': ll_l, 'ranged': range_l,

313 | 'close': close_l})

314 |

315 | except Exception as e:

316 | print(str(e))

317 | ranking_df = []

318 | dfmp_l = []

319 | dist_df = []

320 |

321 | return (dfmp_l, dist_df)

322 |

323 | def get_dayrank(self):

324 | # dist_df = df_distribution_concat.copy()

325 | # LVNs

326 | dist_df = self.get_context()[1]

327 | lvnlist = dist_df['lvnlist'].to_list()

328 | cllist = dist_df['close'].to_list()

329 | lvn_powerlist = []

330 | total_lvns = 0

331 | for c, llist in zip(cllist, lvnlist):

332 | if len(llist) == 0:

333 | delta_lvn = 0

334 | total_lvns = 0

335 | lvn_powerlist.append(total_lvns)

336 | else:

337 | for l in llist:

338 | delta_lvn = c - l

339 | if delta_lvn >= 0:

340 | lvn_i = 1

341 | else:

342 | lvn_i = -1

343 | total_lvns = total_lvns + lvn_i

344 | lvn_powerlist.append(total_lvns)

345 | total_lvns = 0

346 |

347 | dist_df['Single_Prints'] = lvn_powerlist

348 |

349 | dist_df['distr'] = dist_df.tpocount / dist_df.maxtpo

350 | dismean = math.floor(dist_df.distr.mean())

351 | dissig = math.floor(dist_df.distr.std())

352 |

353 | # Assign day types based on TPO distribution and give numerical value for each day types for calculating total strength at the end

354 |

355 | dist_df['daytype'] = np.where(np.logical_and(dist_df.distr >= dismean,

356 | dist_df.distr < dismean + dissig), 'Trend Distribution Day', '')

357 |

358 | dist_df['daytype_num'] = np.where(np.logical_and(dist_df.distr >= dismean,

359 | dist_df.distr < dismean + dissig), 3, 0)

360 |

361 | dist_df['daytype'] = np.where(np.logical_and(dist_df.distr < dismean,

362 | dist_df.distr >= dismean - dissig), 'Normal Variation Day',

363 | dist_df['daytype'])

364 |

365 | dist_df['daytype_num'] = np.where(np.logical_and(dist_df.distr < dismean,

366 | dist_df.distr >= dismean - dissig), 2, dist_df['daytype_num'])

367 |

368 | dist_df['daytype'] = np.where(dist_df.distr < dismean - dissig,

369 | 'Neutral Day', dist_df['daytype'])

370 |

371 | dist_df['daytype_num'] = np.where(dist_df.distr < dismean - dissig,

372 | 1, dist_df['daytype_num'])

373 |

374 | dist_df['daytype'] = np.where(dist_df.distr > dismean + dissig,

375 | 'Trend Day', dist_df['daytype'])

376 | dist_df['daytype_num'] = np.where(dist_df.distr > dismean + dissig,

377 | 4, dist_df['daytype_num'])

378 | dist_df['daytype_num'] = np.where(dist_df.close >= dist_df.poclist, dist_df.daytype_num * 1,

379 | dist_df.daytype_num * -1) # assign signs as per bias

380 |

381 | daytypes = dist_df['daytype'].to_list()

382 |

383 | # volume comparison with mean

384 | mean_val = self.get_mean()

385 | rf_mean = mean_val['rf_mean']

386 | vol_mean = mean_val['volume_mean']

387 |

388 | dist_df['vold_zscore'] = (dist_df.volumed - vol_mean) / dist_df.volumed.std(ddof=0)

389 | dist_df['rfd_zscore'] = (abs(dist_df.rfd) - rf_mean) / abs(dist_df.rfd).std(ddof=0)

390 | a, b = 1, 4

391 | x, y = dist_df.rfd_zscore.min(), dist_df.rfd_zscore.max()

392 | dist_df['norm_rf'] = (dist_df.rfd_zscore - x) / (y - x) * (b - a) + a

393 |

394 | p, q = dist_df.vold_zscore.min(), dist_df.vold_zscore.max()

395 | dist_df['norm_volume'] = (dist_df.vold_zscore - p) / (q - p) * (b - a) + a

396 |

397 | dist_df['volume_Factor'] = np.where(dist_df.close >= dist_df.poclist, dist_df.norm_volume * 1,

398 | dist_df.norm_volume * -1)

399 | dist_df['Rotation_Factor'] = np.where(dist_df.rfd >= 0, dist_df.norm_rf * 1, dist_df.norm_rf * -1)

400 |

401 | # !!! get ranking based on distribution data frame aka dist_df

402 | ranking_df = dist_df.copy()

403 | ranking_df['VAH_vs_yVAH'] = np.where(ranking_df.vahlist >= ranking_df.vahlist.shift(), 1, -1)

404 | ranking_df['VAL_vs_yVAL'] = np.where(ranking_df.vallist >= ranking_df.vallist.shift(), 1, -1)

405 | ranking_df['POC_vs_yPOC'] = np.where(ranking_df.poclist >= ranking_df.poclist.shift(), 1, -1)

406 | ranking_df['H_vs_yH'] = np.where(ranking_df.highd >= ranking_df.highd.shift(), 1, -1)

407 | ranking_df['L_vs_yL'] = np.where(ranking_df.lowd >= ranking_df.lowd.shift(), 1, -1)

408 | ranking_df['Close_vs_yCL'] = np.where(ranking_df.close >= ranking_df.close.shift(), 1, -1)

409 | ranking_df['CL>POC= ranking_df.poclist, ranking_df.close < ranking_df.vahlist), 1, 0)

411 | ranking_df['CLval'] = np.where(

412 | np.logical_and(ranking_df.close < ranking_df.poclist, ranking_df.close >= ranking_df.vallist), -1,

413 | 0) # Max is 2

414 | ranking_df['CL=VAH'] = np.where(ranking_df.close >= ranking_df.vahlist, 2, 0)

416 |

417 | ranking_df['power1'] = 100 * (

418 | (ranking_df.VAH_vs_yVAH + ranking_df.VAL_vs_yVAL + ranking_df.POC_vs_yPOC + ranking_df.H_vs_yH +

419 | ranking_df.L_vs_yL + ranking_df['Close_vs_yCL'] + ranking_df['CL>POCval'] + ranking_df.Single_Prints +

421 | ranking_df['CL=VAH'] + ranking_df.volume_Factor + ranking_df.Rotation_Factor + ranking_df.daytype_num) / 14)

423 |

424 | c, d = 25, 100

425 | r, s = abs(ranking_df.power1).min(), abs(ranking_df.power1).max()

426 | ranking_df['power'] = (abs(ranking_df.power1) - r) / (s - r) * (d - c) + c

427 | ranking_df = ranking_df.round(2)

428 | # ranking_df['power'] = abs(ranking_df['power1'])

429 |

430 | breakdown_df = ranking_df[

431 | ['Single_Prints', 'daytype_num', 'volume_Factor', 'Rotation_Factor', 'VAH_vs_yVAH', 'VAL_vs_yVAL',

432 | 'POC_vs_yPOC', 'H_vs_yH',

433 | 'L_vs_yL', 'Close_vs_yCL', 'CL>POCval', 'CL=VAH']].transpose()

434 |

435 | breakdown_df = breakdown_df.round(2)

436 |

437 | return (ranking_df, breakdown_df)

438 |

--------------------------------------------------------------------------------