├── doc

├── img

│ ├── anac.png

│ ├── anac_m.png

│ ├── jaqs.png

│ ├── analyze.png

│ ├── dataview.png

│ ├── ic_report.png

│ ├── jaqs_test.png

│ ├── anac_ipython.png

│ ├── further_analysis.png

│ ├── returns_report.png

│ ├── backtest_Graham_result.png

│ ├── backtest_ICModel_result.png

│ ├── event_drivent_illustration_dual.png

│ ├── event_drivent_dual_thrust_result.png

│ ├── event_driven_calendar_spread_result.png

│ └── event_driven_roll_within_sector_result.png

├── source

│ ├── modules.rst

│ ├── overview.rst

│ ├── jaqs.research.rst

│ ├── user_guide.rst

│ ├── jaqs.rst

│ ├── api_reference.rst

│ ├── jaqs.trade.event.rst

│ ├── jaqs.trade.analyze.rst

│ ├── index.rst

│ ├── jaqs.data.dataapi.rst

│ ├── jaqs.trade.tradeapi.rst

│ ├── jaqs.research.signaldigger.rst

│ ├── md2rst.py

│ ├── jaqs.data.basic.rst

│ ├── jaqs.util.rst

│ ├── jaqs.data.rst

│ ├── jaqs.trade.rst

│ ├── how_to_ask_questions.rst

│ ├── research.rst

│ ├── base_data.rst

│ ├── realtime.rst

│ ├── trade_api.rst

│ └── install.rst

├── overview.md

├── data_api.md

├── base_data.md

├── how_to_ask_questions.md

├── research.md

├── realtime.md

├── Makefile

├── install.md

└── trade_api.md

├── MANIFEST.in

├── publish

├── publish_pypi.sh

└── publish_conda.sh

├── requirements.txt

├── example

├── alpha

│ ├── __init__.py

│ ├── config_path.py

│ ├── single_factor_weight.py

│ ├── wine_industry_momentum.py

│ ├── select_stocks_pe_profit.py

│ ├── select_stocks_industry_head.py

│ ├── FamaFrench.py

│ └── first_example.py

├── eventdriven

│ ├── __init__.py

│ ├── config_path.py

│ ├── custom_symbol_signal.py

│ ├── CalendarSpread.py

│ └── market_making.py

└── research

│ ├── config_path.py

│ ├── signal_return_ic_analysis_single.py

│ ├── event_analysis.py

│ └── signal_return_ic_analysis.py

├── jaqs

├── research

│ ├── __init__.py

│ └── signaldigger

│ │ └── __init__.py

├── util

│ ├── __init__.py

│ ├── sequence.py

│ ├── numeric.py

│ ├── pdutil.py

│ ├── profile.py

│ ├── fileio.py

│ └── dtutil.py

├── trade

│ ├── analyze

│ │ ├── static

│ │ │ ├── test_template.html

│ │ │ ├── additional.css

│ │ │ └── bootstrap-toc

│ │ │ │ ├── bootstrap-toc.min.css

│ │ │ │ └── bootstrap-toc.min.js

│ │ ├── __init__.py

│ │ └── report.py

│ ├── event

│ │ ├── __init__.py

│ │ └── eventtype.py

│ ├── tradeapi

│ │ ├── __init__.py

│ │ ├── README.md

│ │ ├── .gitignore

│ │ └── utils.py

│ ├── __init__.py

│ └── common.py

├── __init__.py

└── data

│ ├── dataapi

│ ├── __init__.py

│ ├── README.md

│ ├── .gitignore

│ └── utils.py

│ ├── __init__.py

│ ├── basic

│ ├── __init__.py

│ ├── instrument.py

│ ├── position.py

│ └── trade.py

│ ├── align.py

│ └── continue_contract.py

├── requirements_doc.txt

├── .gitattributes

├── requirements_test.txt

├── config

├── trade_config.json

└── data_config.json

├── test

├── test_model.py

├── test_sequence_generator.py

├── config_path.py

├── test_report.py

├── test_strategy.py

├── test_data_api.py

├── test_research.py

├── test_align.py

├── test_backtest_alpha.py

└── test_trade_api.py

├── .travis.yml

├── .gitignore

├── setup.py

├── README.rst

└── TODO.md

/doc/img/anac.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/anac.png

--------------------------------------------------------------------------------

/doc/img/anac_m.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/anac_m.png

--------------------------------------------------------------------------------

/doc/img/jaqs.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/jaqs.png

--------------------------------------------------------------------------------

/doc/img/analyze.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/analyze.png

--------------------------------------------------------------------------------

/doc/img/dataview.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/dataview.png

--------------------------------------------------------------------------------

/doc/img/ic_report.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/ic_report.png

--------------------------------------------------------------------------------

/doc/img/jaqs_test.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/jaqs_test.png

--------------------------------------------------------------------------------

/MANIFEST.in:

--------------------------------------------------------------------------------

1 | include requirements.txt

2 | recursive-include jaqs/trade/analyze/static *.js *.html *.css

--------------------------------------------------------------------------------

/doc/img/anac_ipython.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/anac_ipython.png

--------------------------------------------------------------------------------

/doc/source/modules.rst:

--------------------------------------------------------------------------------

1 | jaqs

2 | ====

3 |

4 | .. toctree::

5 | :maxdepth: 4

6 |

7 | jaqs

8 |

--------------------------------------------------------------------------------

/doc/img/further_analysis.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/further_analysis.png

--------------------------------------------------------------------------------

/doc/img/returns_report.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/returns_report.png

--------------------------------------------------------------------------------

/publish/publish_pypi.sh:

--------------------------------------------------------------------------------

1 | python setup.py sdist

2 | python setup.py bdist_wheel --universal

3 | twine upload dist/*

4 |

--------------------------------------------------------------------------------

/doc/img/backtest_Graham_result.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/backtest_Graham_result.png

--------------------------------------------------------------------------------

/doc/img/backtest_ICModel_result.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/backtest_ICModel_result.png

--------------------------------------------------------------------------------

/requirements.txt:

--------------------------------------------------------------------------------

1 | future

2 | Jinja2

3 | msgpack-python

4 | pandas >= 0.20.0

5 | pyzmq

6 | python-snappy

7 | seaborn

8 | six

9 |

--------------------------------------------------------------------------------

/doc/overview.md:

--------------------------------------------------------------------------------

1 |

2 | ## Overview

3 |

4 | 框架概览:

5 |

6 | - 使用数据API,轻松获取研究数据

7 | - 根据策略模板,编写自己的量化策略

8 | - 使用回测框架,对策略进行回测和验证

9 |

--------------------------------------------------------------------------------

/doc/img/event_drivent_illustration_dual.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/event_drivent_illustration_dual.png

--------------------------------------------------------------------------------

/example/alpha/__init__.py:

--------------------------------------------------------------------------------

1 | # encoding: UTF-8

2 | """

3 | The example module contains several examples of using py-hft-trade.

4 | """

5 |

--------------------------------------------------------------------------------

/jaqs/research/__init__.py:

--------------------------------------------------------------------------------

1 | # encoding: utf-8

2 |

3 | from .signaldigger import SignalDigger

4 |

5 |

6 | __all__ = ['SignalDigger']

7 |

--------------------------------------------------------------------------------

/doc/img/event_drivent_dual_thrust_result.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/event_drivent_dual_thrust_result.png

--------------------------------------------------------------------------------

/doc/source/overview.rst:

--------------------------------------------------------------------------------

1 | Overview

2 | --------

3 |

4 | 框架概览:

5 |

6 | - 使用数据API,轻松获取研究数据

7 | - 根据策略模板,编写自己的量化策略

8 | - 使用回测框架,对策略进行回测和验证

9 |

--------------------------------------------------------------------------------

/example/eventdriven/__init__.py:

--------------------------------------------------------------------------------

1 | # encoding: UTF-8

2 | """

3 | The example module contains several examples of using py-hft-trade.

4 | """

5 |

--------------------------------------------------------------------------------

/jaqs/research/signaldigger/__init__.py:

--------------------------------------------------------------------------------

1 | # encoding: utf-8

2 |

3 | from .digger import SignalDigger

4 |

5 |

6 | __all__ = ['SignalDigger']

7 |

--------------------------------------------------------------------------------

/doc/img/event_driven_calendar_spread_result.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/event_driven_calendar_spread_result.png

--------------------------------------------------------------------------------

/doc/img/event_driven_roll_within_sector_result.png:

--------------------------------------------------------------------------------

https://raw.githubusercontent.com/quantOS-org/JAQS/HEAD/doc/img/event_driven_roll_within_sector_result.png

--------------------------------------------------------------------------------

/requirements_doc.txt:

--------------------------------------------------------------------------------

1 | future

2 | enum34

3 | Jinja2

4 | msgpack_python

5 | pandas >= 0.20.0

6 | pyzmq

7 | seaborn

8 | six

9 | sphinx_rtd_theme

10 |

--------------------------------------------------------------------------------

/jaqs/util/__init__.py:

--------------------------------------------------------------------------------

1 | # encoding: utf-8

2 |

3 | from .dtutil import *

4 | from .fileio import *

5 | from .numeric import *

6 | from .pdutil import *

7 | from .profile import *

8 | from .sequence import *

9 |

--------------------------------------------------------------------------------

/publish/publish_conda.sh:

--------------------------------------------------------------------------------

1 | conda skeleton pypi jaqs

2 | cp build1.sh jaqs

3 | grep -rl "^.*enum34.*$" jaqs | xargs sed -i "s|^.*enum34.*$||g"

4 | conda config --set anaconda_upload yes

5 | conda-build jaqs

6 |

--------------------------------------------------------------------------------

/.gitattributes:

--------------------------------------------------------------------------------

1 | *.js linguist-language=Python

2 | *.css linguist-language=Python

3 | *.html linguist-language=Python

4 | *.ipynb linguist-language=Python

5 | *.md linguist-language=Python

6 | *.png linguist-language=Python

7 |

--------------------------------------------------------------------------------

/requirements_test.txt:

--------------------------------------------------------------------------------

1 | future

2 | enum34

3 | Jinja2

4 | msgpack_python

5 | pandas >= 0.20.0

6 | pytest

7 | pytest-cov

8 | python-coveralls

9 | python-snappy

10 | pyzmq

11 | seaborn

12 | six

13 | sphinx_rtd_theme

14 |

--------------------------------------------------------------------------------

/jaqs/trade/analyze/static/test_template.html:

--------------------------------------------------------------------------------

1 |

2 |

3 |

4 |

5 | {{ mytitle }}

6 |

7 |

8 | Sales Funnel Report - National

9 | {{ mytable }}

10 |

11 |

--------------------------------------------------------------------------------

/config/trade_config.json:

--------------------------------------------------------------------------------

1 | {

2 | "remote.trade.address": "tcp://gw.quantos.org:8901",

3 | "remote.trade.username": "17621969269",

4 | "remote.trade.password": "eyJhbGciOiJIUzI1NiJ9.eyJjcmVhdGVfdGltZSI6IjE1MTIwMjA0OTQwMzciLCJpc3MiOiJhdXRoMCIsImlkIjoiMTc2MjE5NjkyNjkifQ.WQvI9k6dvXe5zIzQwyuPI4BM0Py1OSYFENIQ3z0RG6c"

5 | }

--------------------------------------------------------------------------------

/jaqs/util/sequence.py:

--------------------------------------------------------------------------------

1 | # encoding: utf-8

2 |

3 | from collections import defaultdict

4 |

5 |

6 | class SequenceGenerator(object):

7 | def __init__(self):

8 | self.__d = defaultdict(int)

9 |

10 | def get_next(self, key):

11 | self.__d[key] += 1

12 | return self.__d[key]

13 |

--------------------------------------------------------------------------------

/config/data_config.json:

--------------------------------------------------------------------------------

1 | {

2 | "remote.data.address": "tcp://data.quantos.org:8910",

3 | "remote.data.username": "17621969269",

4 | "remote.data.password": "eyJhbGciOiJIUzI1NiJ9.eyJjcmVhdGVfdGltZSI6IjE1MTIwMjA0OTQwMzciLCJpc3MiOiJhdXRoMCIsImlkIjoiMTc2MjE5NjkyNjkifQ.WQvI9k6dvXe5zIzQwyuPI4BM0Py1OSYFENIQ3z0RG6c"

5 | }

6 |

--------------------------------------------------------------------------------

/doc/source/jaqs.research.rst:

--------------------------------------------------------------------------------

1 | jaqs\.research package

2 | ======================

3 |

4 | Subpackages

5 | -----------

6 |

7 | .. toctree::

8 |

9 | jaqs.research.signaldigger

10 |

11 | Module contents

12 | ---------------

13 |

14 | .. automodule:: jaqs.research

15 | :members:

16 | :undoc-members:

17 | :show-inheritance:

18 |

--------------------------------------------------------------------------------

/doc/source/user_guide.rst:

--------------------------------------------------------------------------------

1 | 用户手册

2 | ========

3 |

4 | 本页面给用户提供了一个简洁清晰的入门指南,涵盖各个功能模块

5 |

6 | .. include:: overview.rst

7 |

8 | .. include:: data_api.rst

9 |

10 | .. include:: data_view.rst

11 |

12 | .. include:: research.rst

13 |

14 | .. include:: backtest.rst

15 |

16 | .. include:: trade_api.rst

17 |

18 | .. include:: realtime.rst

19 |

--------------------------------------------------------------------------------

/doc/source/jaqs.rst:

--------------------------------------------------------------------------------

1 | jaqs package

2 | ============

3 |

4 | Subpackages

5 | -----------

6 |

7 | .. toctree::

8 |

9 | jaqs.data

10 | jaqs.research

11 | jaqs.trade

12 | jaqs.util

13 |

14 | Module contents

15 | ---------------

16 |

17 | .. automodule:: jaqs

18 | :members:

19 | :undoc-members:

20 | :show-inheritance:

21 |

--------------------------------------------------------------------------------

/jaqs/trade/event/__init__.py:

--------------------------------------------------------------------------------

1 | # encoding: UTF-8

2 | """

3 | The event processing engine is where the event is identified,

4 | and the appropriate reaction is selected and executed.

5 |

6 | Our framework utilizes event engine to run in an efficient way.

7 |

8 | """

9 | from .engine import EventEngine, Event

10 | from .eventtype import EVENT_TYPE

11 |

--------------------------------------------------------------------------------

/test/test_model.py:

--------------------------------------------------------------------------------

1 | # encoding: utf-8

2 |

3 | from __future__ import absolute_import, division, print_function

4 |

5 | from jaqs.trade import model

6 |

7 |

8 | def test_model():

9 | model.StockSelector()

10 | model.SimpleCostModel()

11 | model.AlphaContext()

12 | model.FactorRiskModel()

13 | model.FactorSignalModel()

14 |

--------------------------------------------------------------------------------

/jaqs/__init__.py:

--------------------------------------------------------------------------------

1 | # encoding: utf-8

2 | """

3 | JAQS

4 | ~~~~

5 |

6 | Open source quantitative research&trading framework.

7 |

8 | copyright: (c) 2017 quantOS-org.

9 | license: Apache 2.0, see LICENSE for details.

10 | """

11 |

12 | import os

13 |

14 |

15 | __version__ = '0.6.14'

16 | SOURCE_ROOT_DIR = os.path.dirname(os.path.abspath(__file__))

17 |

--------------------------------------------------------------------------------

/jaqs/data/dataapi/__init__.py:

--------------------------------------------------------------------------------

1 | # encoding: utf-8

2 | """

3 | dataapi defines standard APIs for communicating with data service.

4 |

5 | """

6 | from __future__ import absolute_import

7 | from __future__ import division

8 | from __future__ import print_function

9 | from __future__ import unicode_literals

10 |

11 | from .data_api import DataApi

12 |

13 | __all__ = ['DataApi']

14 |

--------------------------------------------------------------------------------

/jaqs/trade/tradeapi/__init__.py:

--------------------------------------------------------------------------------

1 | # encoding: utf-8

2 | """

3 | tradeapi defines standard APIs for communicating with

4 | algorithmic trading & executing system.

5 | """

6 | from __future__ import absolute_import

7 | from __future__ import division

8 | from __future__ import print_function

9 | from __future__ import unicode_literals

10 |

11 | from .trade_api import TradeApi

12 |

13 | __all__ = ['TradeApi']

14 |

--------------------------------------------------------------------------------

/.travis.yml:

--------------------------------------------------------------------------------

1 | language: python

2 |

3 | python:

4 | - "2.7"

5 | - "3.6"

6 |

7 | branches:

8 | only:

9 | - master

10 |

11 | before_install:

12 | - sudo apt-get -qq update

13 | - sudo apt-get install -y libsnappy-dev

14 |

15 | install:

16 | - pip install -r requirements_test.txt

17 |

18 | before_script:

19 | - python setup.py install

20 |

21 | script:

22 | - cd test

23 | - py.test test_util.py --cov jaqs

24 |

25 |

--------------------------------------------------------------------------------

/jaqs/data/__init__.py:

--------------------------------------------------------------------------------

1 | # encoding: utf-8

2 |

3 | """

4 | Modules relevant to data.

5 |

6 | """

7 |

8 | from .dataapi import DataApi

9 | from .dataservice import RemoteDataService, DataService

10 | from .dataview import DataView, EventDataView

11 | from .py_expression_eval import Parser

12 |

13 |

14 | # we do not expose align and basic

15 | __all__ = ['DataApi', 'DataService', 'RemoteDataService', 'DataView', 'Parser', 'EventDataView']

--------------------------------------------------------------------------------

/doc/source/api_reference.rst:

--------------------------------------------------------------------------------

1 | API说明文档

2 | ============

3 |

4 | 行情数据API文档

5 | ---------------

6 | .. toctree::

7 | :maxdepth: 2

8 |

9 | market_data

10 |

11 |

12 | 参考数据API文档

13 | ---------------

14 | .. toctree::

15 | :maxdepth: 2

16 |

17 | base_data

18 |

19 |

20 | Other Important APIs

21 | --------------------

22 |

23 | .. toctree::

24 | :maxdepth: 2

25 |

26 | jaqs.data

27 | jaqs.trade

28 | jaqs.research

29 | jaqs.util

30 |

--------------------------------------------------------------------------------

/test/test_sequence_generator.py:

--------------------------------------------------------------------------------

1 | # encoding: utf-8

2 | from jaqs.util.sequence import SequenceGenerator

3 |

4 |

5 | def test_seq_gen():

6 | sg = SequenceGenerator()

7 | for i in range(1, 999):

8 | assert sg.get_next('order') == i

9 |

10 | text = 'trade'

11 | sg.get_next(text)

12 | sg.get_next(text)

13 | for i in range(3, 999):

14 | assert sg.get_next(text) == i

15 |

16 |

17 | if __name__ == "__main__":

18 | test_seq_gen()

19 |

--------------------------------------------------------------------------------

/test/config_path.py:

--------------------------------------------------------------------------------

1 | # encoding: UTF-8

2 |

3 | from __future__ import print_function

4 | import os

5 |

6 |

7 | _test_dir = os.path.dirname(os.path.abspath(__file__))

8 | DATA_CONFIG_PATH = os.path.abspath(os.path.join(_test_dir, '../config/data_config.json'))

9 | TRADE_CONFIG_PATH = os.path.abspath(os.path.join(_test_dir, '../config/trade_config.json'))

10 |

11 | print("Current data config file path: {}".format(DATA_CONFIG_PATH))

12 | print("Current trade config file path: {}".format(TRADE_CONFIG_PATH))

13 |

--------------------------------------------------------------------------------

/example/alpha/config_path.py:

--------------------------------------------------------------------------------

1 | # encoding: UTF-8

2 |

3 | from __future__ import print_function

4 | import os

5 |

6 |

7 | _test_dir = os.path.dirname(os.path.abspath(__file__))

8 | DATA_CONFIG_PATH = os.path.abspath(os.path.join(_test_dir, '../../config/data_config.json'))

9 | TRADE_CONFIG_PATH = os.path.abspath(os.path.join(_test_dir, '../../config/trade_config.json'))

10 |

11 | print("Current data config file path: {}".format(DATA_CONFIG_PATH))

12 | print("Current trade config file path: {}".format(TRADE_CONFIG_PATH))

13 |

--------------------------------------------------------------------------------

/example/research/config_path.py:

--------------------------------------------------------------------------------

1 | # encoding: UTF-8

2 |

3 | from __future__ import print_function

4 | import os

5 |

6 |

7 | _test_dir = os.path.dirname(os.path.abspath(__file__))

8 | DATA_CONFIG_PATH = os.path.abspath(os.path.join(_test_dir, '../../config/data_config.json'))

9 | TRADE_CONFIG_PATH = os.path.abspath(os.path.join(_test_dir, '../../config/trade_config.json'))

10 |

11 | print("Current data config file path: {}".format(DATA_CONFIG_PATH))

12 | print("Current trade config file path: {}".format(TRADE_CONFIG_PATH))

13 |

--------------------------------------------------------------------------------

/example/eventdriven/config_path.py:

--------------------------------------------------------------------------------

1 | # encoding: UTF-8

2 |

3 | from __future__ import print_function

4 | import os

5 |

6 |

7 | _test_dir = os.path.dirname(os.path.abspath(__file__))

8 | DATA_CONFIG_PATH = os.path.abspath(os.path.join(_test_dir, '../../config/data_config.json'))

9 | TRADE_CONFIG_PATH = os.path.abspath(os.path.join(_test_dir, '../../config/trade_config.json'))

10 |

11 | print("Current data config file path: {}".format(DATA_CONFIG_PATH))

12 | print("Current trade config file path: {}".format(TRADE_CONFIG_PATH))

13 |

--------------------------------------------------------------------------------

/doc/data_api.md:

--------------------------------------------------------------------------------

1 | ## 数据API

2 |

3 | 本产品提供了金融数据api,方便用户调用接口获取各种数据,通过python的api调用接口,返回DataFrame格式的数据和消息,以下是用法

4 |

5 | ### 导入接口

6 |

7 | 在python程序里面导入module,然后用注册的用户帐号登录就可以使用行情和参考数据的接口来获取数据了

8 |

9 | #### 引入模块

10 |

11 | ```python

12 | from jaqs.data import DataApi

13 | ```

14 | #### 登录数据服务器

15 | ```python

16 | api = DataApi(addr='tcp://data.quantos.org:8910')

17 | api.login(phone, token)

18 | ```

19 |

20 | ### 调用数据接口

21 |

22 | 主要数据主要分为两大类:

23 |

24 | - **市场数据**,目前可使用的数据包括日线,分钟线,实时行情等。

25 | - **参考数据**,包括财务数据、公司行为数据、指数成份数据等。

26 |

27 | 数据API使用方法参考下面的数据API说明。

28 |

29 |

--------------------------------------------------------------------------------

/test/test_report.py:

--------------------------------------------------------------------------------

1 | # encoding: utf-8

2 | from jaqs.trade.analyze.report import Report

3 | import jaqs.util as jutil

4 |

5 |

6 | def test_output():

7 | static_folder = jutil.join_relative_path('trade/analyze/static')

8 |

9 | r = Report({'mytitle': 'Test Title', 'mytable': 'Hello World!'},

10 | source_dir=static_folder,

11 | template_fn='test_template.html',

12 | out_folder='../output')

13 | r.generate_html()

14 | r.output_html()

15 | r.output_pdf()

16 |

17 |

18 | if __name__ == "__main__":

19 | test_output()

20 |

--------------------------------------------------------------------------------

/doc/source/jaqs.trade.event.rst:

--------------------------------------------------------------------------------

1 | jaqs\.trade\.event package

2 | ==========================

3 |

4 | Submodules

5 | ----------

6 |

7 | jaqs\.trade\.event\.engine module

8 | ---------------------------------

9 |

10 | .. automodule:: jaqs.trade.event.engine

11 | :members:

12 | :undoc-members:

13 | :show-inheritance:

14 |

15 | jaqs\.trade\.event\.eventtype module

16 | ------------------------------------

17 |

18 | .. automodule:: jaqs.trade.event.eventtype

19 | :members:

20 | :undoc-members:

21 | :show-inheritance:

22 |

23 |

24 | Module contents

25 | ---------------

26 |

27 | .. automodule:: jaqs.trade.event

28 | :members:

29 | :undoc-members:

30 | :show-inheritance:

31 |

--------------------------------------------------------------------------------

/jaqs/trade/analyze/__init__.py:

--------------------------------------------------------------------------------

1 | """

2 | Classes defined in analyze module help automate analysis of trading results.

3 |

4 | It takes a CSV file, trades.csv, which contains trading records, and a JSON file,

5 | configs.json, which contains some necessary configurations. Then it can automatically

6 | calculate PnL, position and various trade statistics and generate an HTML report.

7 |

8 | Usage:

9 | ta.initialize(dataview=dv, file_folder=backtest_result_dir_path)

10 | ta.do_analyze(result_dir=backtest_result_dir_path, selected_sec=list(ta.universe)[:3], brinson_group='sw1')

11 | """

12 |

13 | from .analyze import EventAnalyzer, AlphaAnalyzer

14 |

15 |

16 | __all__ = ['EventAnalyzer', 'AlphaAnalyzer']

--------------------------------------------------------------------------------

/doc/source/jaqs.trade.analyze.rst:

--------------------------------------------------------------------------------

1 | jaqs\.trade\.analyze package

2 | ============================

3 |

4 | Submodules

5 | ----------

6 |

7 | jaqs\.trade\.analyze\.analyze module

8 | ------------------------------------

9 |

10 | .. automodule:: jaqs.trade.analyze.analyze

11 | :members:

12 | :undoc-members:

13 | :show-inheritance:

14 |

15 | jaqs\.trade\.analyze\.report module

16 | -----------------------------------

17 |

18 | .. automodule:: jaqs.trade.analyze.report

19 | :members:

20 | :undoc-members:

21 | :show-inheritance:

22 |

23 |

24 | Module contents

25 | ---------------

26 |

27 | .. automodule:: jaqs.trade.analyze

28 | :members:

29 | :undoc-members:

30 | :show-inheritance:

31 |

--------------------------------------------------------------------------------

/jaqs/trade/__init__.py:

--------------------------------------------------------------------------------

1 | # encoding: UTF-8

2 | """

3 | Basic data types, classes and models for trade.

4 |

5 | """

6 |

7 | from .tradeapi import TradeApi

8 | from .backtest import AlphaBacktestInstance, EventBacktestInstance

9 | from .portfoliomanager import PortfolioManager

10 | from .livetrade import EventLiveTradeInstance, AlphaLiveTradeInstance

11 | from .strategy import Strategy, AlphaStrategy, EventDrivenStrategy

12 | from .tradegateway import BaseTradeApi, RealTimeTradeApi, AlphaTradeApi, BacktestTradeApi

13 |

14 |

15 | __all__ = ['TradeApi',

16 | 'AlphaBacktestInstance', 'EventBacktestInstance',

17 | 'PortfolioManager',

18 | 'EventLiveTradeInstance', 'AlphaLiveTradeInstance',

19 | 'Strategy', 'AlphaStrategy', 'EventDrivenStrategy',

20 | 'BaseTradeApi', 'RealTimeTradeApi', 'AlphaTradeApi', 'BacktestTradeApi']

21 |

--------------------------------------------------------------------------------

/doc/source/index.rst:

--------------------------------------------------------------------------------

1 |

2 | JAQS

3 | ==========================================================

4 |

5 | 在这里,你将可以获得:

6 |

7 | - 使用数据API,轻松获取研究数据

8 | - 根据策略模板,编写自己的量化策略

9 | - 使用回测框架,对策略进行回测和验证

10 |

11 | 查看代码,请点击\ `GitHub `__\

12 |

13 | Install Guide

14 | -------------

15 |

16 | A detailed step-by-step description of installation.

17 |

18 | .. toctree::

19 | :maxdepth: 2

20 |

21 | install

22 |

23 |

24 | 用户手册

25 | -------------

26 |

27 | 一个简洁清晰的入门指南, 涵盖各个功能模块.

28 |

29 | .. toctree::

30 | :maxdepth: 2

31 |

32 | user_guide

33 |

34 |

35 | API Refrence

36 | -------------

37 |

38 | If you want to know about package hierarchy, specific class / function...

39 |

40 | .. toctree::

41 | :maxdepth: 2

42 |

43 | api_reference

44 |

45 |

46 | License

47 | -------

48 |

49 | Apache 2.0许可协议。版权所有(c)2017 quantOS-org(量化开源会)。

50 |

--------------------------------------------------------------------------------

/doc/source/jaqs.data.dataapi.rst:

--------------------------------------------------------------------------------

1 | jaqs\.data\.dataapi package

2 | ===========================

3 |

4 | Submodules

5 | ----------

6 |

7 | jaqs\.data\.dataapi\.data\_api module

8 | -------------------------------------

9 |

10 | .. automodule:: jaqs.data.dataapi.data_api

11 | :members:

12 | :undoc-members:

13 | :show-inheritance:

14 |

15 | jaqs\.data\.dataapi\.jrpc\_py module

16 | ------------------------------------

17 |

18 | .. automodule:: jaqs.data.dataapi.jrpc_py

19 | :members:

20 | :undoc-members:

21 | :show-inheritance:

22 |

23 | jaqs\.data\.dataapi\.utils module

24 | ---------------------------------

25 |

26 | .. automodule:: jaqs.data.dataapi.utils

27 | :members:

28 | :undoc-members:

29 | :show-inheritance:

30 |

31 |

32 | Module contents

33 | ---------------

34 |

35 | .. automodule:: jaqs.data.dataapi

36 | :members:

37 | :undoc-members:

38 | :show-inheritance:

39 |

--------------------------------------------------------------------------------

/jaqs/trade/analyze/static/additional.css:

--------------------------------------------------------------------------------

1 | img {

2 | max-width: 80%;

3 | max-height: 80%;

4 | }

5 | body {

6 | background-color: #FBFBFB !important;

7 | }

8 | table {

9 | width: auto !important;

10 | }

11 |

12 | h2 {

13 | margin: 3em 0 0.5em 0 !important;

14 | padding: 5px 15px !important;

15 | color: white !important;

16 | background: #476EA1 !important;

17 | border: 1px solid #fff !important;

18 | border-radius: 0 10px 0 10px !important;

19 | }

20 | h3 {

21 | margin: 1em 0 0.5em 0 !important;

22 | padding: 5px 15px !important;

23 | }

24 |

25 | .right-bottom {

26 | position: fixed;

27 | right: 5em;

28 | bottom: 1em;

29 | }

30 |

31 | #mytoc {

32 | position: fixed;

33 | right: 0;

34 | top: 0;

35 | background-color:#FFF;

36 | }

37 |

38 | #mytoc #full { display: none; } /* Hide the full TOC by default */

39 |

40 | #mytoc:hover #full{

41 | display: block; /* Show it on hover */

42 | }

--------------------------------------------------------------------------------

/doc/source/jaqs.trade.tradeapi.rst:

--------------------------------------------------------------------------------

1 | jaqs\.trade\.tradeapi package

2 | =============================

3 |

4 | Submodules

5 | ----------

6 |

7 | jaqs\.trade\.tradeapi\.jrpc\_py module

8 | --------------------------------------

9 |

10 | .. automodule:: jaqs.trade.tradeapi.jrpc_py

11 | :members:

12 | :undoc-members:

13 | :show-inheritance:

14 |

15 | jaqs\.trade\.tradeapi\.trade\_api module

16 | ----------------------------------------

17 |

18 | .. automodule:: jaqs.trade.tradeapi.trade_api

19 | :members:

20 | :undoc-members:

21 | :show-inheritance:

22 |

23 | jaqs\.trade\.tradeapi\.utils module

24 | -----------------------------------

25 |

26 | .. automodule:: jaqs.trade.tradeapi.utils

27 | :members:

28 | :undoc-members:

29 | :show-inheritance:

30 |

31 |

32 | Module contents

33 | ---------------

34 |

35 | .. automodule:: jaqs.trade.tradeapi

36 | :members:

37 | :undoc-members:

38 | :show-inheritance:

39 |

--------------------------------------------------------------------------------

/doc/source/jaqs.research.signaldigger.rst:

--------------------------------------------------------------------------------

1 | jaqs\.research\.signaldigger package

2 | ====================================

3 |

4 | Submodules

5 | ----------

6 |

7 | jaqs\.research\.signaldigger\.digger module

8 | -------------------------------------------

9 |

10 | .. automodule:: jaqs.research.signaldigger.digger

11 | :members:

12 | :undoc-members:

13 | :show-inheritance:

14 |

15 | jaqs\.research\.signaldigger\.performance module

16 | ------------------------------------------------

17 |

18 | .. automodule:: jaqs.research.signaldigger.performance

19 | :members:

20 | :undoc-members:

21 | :show-inheritance:

22 |

23 | jaqs\.research\.signaldigger\.plotting module

24 | ---------------------------------------------

25 |

26 | .. automodule:: jaqs.research.signaldigger.plotting

27 | :members:

28 | :undoc-members:

29 | :show-inheritance:

30 |

31 |

32 | Module contents

33 | ---------------

34 |

35 | .. automodule:: jaqs.research.signaldigger

36 | :members:

37 | :undoc-members:

38 | :show-inheritance:

39 |

--------------------------------------------------------------------------------

/test/test_strategy.py:

--------------------------------------------------------------------------------

1 | # encoding: utf-8

2 |

3 | from __future__ import print_function

4 | from jaqs.trade import model

5 | import jaqs.util as jutil

6 | import random

7 |

8 |

9 | def test_context():

10 | r = random.random()

11 | path = '../../output/tests/storage{:.6f}.pic'.format(r)

12 | context = model.Context()

13 | context.load_store(path)

14 | assert len(context.storage) == 0

15 | context.storage['me'] = 1.0

16 | context.save_store(path)

17 |

18 | context = model.Context()

19 | context.load_store(path)

20 | assert context.storage['me'] == 1.0

21 |

22 |

23 | if __name__ == "__main__":

24 | import time

25 | t_start = time.time()

26 |

27 | g = globals()

28 | g = {k: v for k, v in g.items() if k.startswith('test_') and callable(v)}

29 |

30 | for test_name, test_func in g.items():

31 | print("\n==========\nTesting {:s}...".format(test_name))

32 | test_func()

33 | print("Test Complete.")

34 |

35 | t3 = time.time() - t_start

36 | print("\n\n\nTime lapsed in total: {:.1f}".format(t3))

37 |

--------------------------------------------------------------------------------

/jaqs/data/dataapi/README.md:

--------------------------------------------------------------------------------

1 | # DataApi

2 |

3 | 标准数据API定义。

4 |

5 | # 安装步骤

6 |

7 | ## 1、安装Python环境

8 |

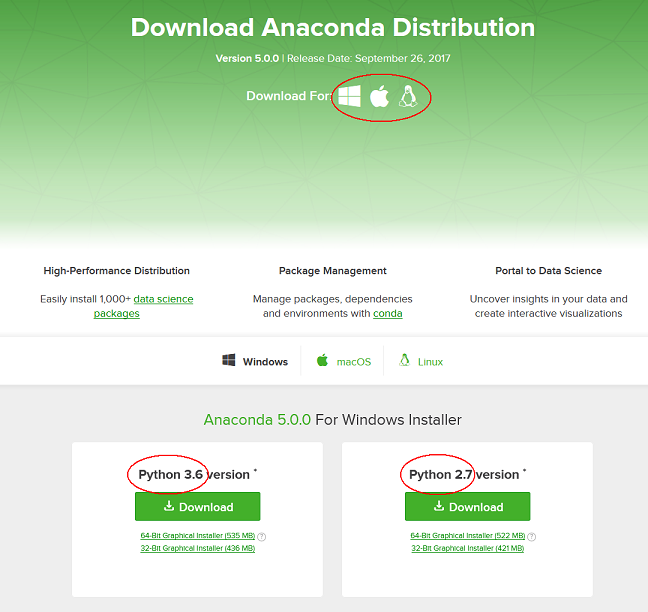

9 | 如果本地还没有安装Python环境,强烈建议安装Anaconda(Python的集成开发环境,包含众多常用包,且易于安装,避免不必要的麻烦)。打开[Anaconda官网](http://www.continuum.io/downloads),选择相应的操作系统,确定要安装的Python版本,进行下载。

10 |

11 | 下载完成以后,按照图形界面步骤完成安装。在默认情况下,Anaconda会自动设置PATH环境。

12 |

13 | ***注***:如果安装过程遇到问题,或需要更详细的步骤,请参见[安装Anaconda Python环境教程](https://github.com/quantOS-org/JAQS/blob/master/doc/install.md#1安装python环境)

14 |

15 | ## 2、安装依赖包

16 |

17 | 如果Python环境不是类似Anaconda的集成开发环境,我们需要单独安装依赖包,在已经有pandas/numpy包前提下,还需要有以下几个包:

18 | - `pyzmq`

19 | - `msgpack_python`

20 | - `python-snappy`

21 |

22 | 可以通过单个安装完成,例如: `pip install pyzmq`

23 |

24 | 需要注意的是,`python-snappy`的安装需要比较多的编译依赖,请按照[如何安装python-snappy包](https://github.com/quantOS-org/JAQS/blob/master/doc/install.md#如何安装python-snappy包)所述安装。

25 |

26 |

27 | ## 3、使用DataApi

28 |

29 | ```python

30 | from DataApi import DataApi # 这里假设项目目录名为DataApi, 且存放在工作目录下

31 |

32 | api = DataApi(addr="tcp://data.quantos.org:8910")

33 | result, msg = api.login("phone", "token") # 示例账户,用户需要改为自己在www.quantos.org上注册的账户

34 | print(result)

35 | print(msg)

36 | ```

37 |

38 |

--------------------------------------------------------------------------------

/jaqs/data/basic/__init__.py:

--------------------------------------------------------------------------------

1 | # encoding: utf-8

2 | """

3 | jaqs.data.basic module includes basic definitions of basic data types

4 | that are used across jaqs package.

5 |

6 | Basic data types:

7 | - `Instrument`: An Instrument represents a specific financial contract.

8 | - `InstManager`: InstManager query information of instruments from data server and store them.

9 | - `Bar`: A Bar is a summary of information of price and volume during a certain length of time span.

10 | - `Quote`: Quote represents a snapshot of price and volume information.

11 | - `Order`: Basic order class.

12 | - `OrderStatusInd`: OrderStatusInd is a indication of status change of an order.

13 | - `Task`: Task is a high-level trading target, which may contain many orders.

14 | - `Position`: Basic position class.

15 | - `Trade`: Trade represents fill/partial fill of an order.

16 | - `TradeInd`: TaskInd is a indication of status change of a task.

17 | - `TradeStat`: TradeStat stores statistics of trading of a certain symbol.

18 |

19 | """

20 | from .marketdata import *

21 | from .order import *

22 | from .trade import *

23 | from .position import *

24 | from .instrument import *

25 |

--------------------------------------------------------------------------------

/jaqs/trade/tradeapi/README.md:

--------------------------------------------------------------------------------

1 | # TradeApi

2 |

3 | 标准交易API定义

4 |

5 | # 安装步骤

6 |

7 | ## 1、安装Python环境

8 |

9 | 如果本地还没有安装Python环境,强烈建议安装Anaconda(Python的集成开发环境,包含众多常用包,且易于安装,避免不必要的麻烦)。打开[Anaconda官网](http://www.continuum.io/downloads),选择相应的操作系统,确定要安装的Python版本,进行下载。

10 |

11 | 下载完成以后,按照图形界面步骤完成安装。在默认情况下,Anaconda会自动设置PATH环境。

12 |

13 | ***注***:如果安装过程遇到问题,或需要更详细的步骤,请参见[安装Anaconda Python环境教程](https://github.com/quantOS-org/JAQS/blob/master/doc/install.md#1安装python环境)

14 |

15 | ## 2、安装依赖包

16 |

17 | 如果Python环境不是类似Anaconda的集成开发环境,我们需要单独安装依赖包,在已经有pandas/numpy包前提下,还需要有以下几个包:

18 | - `pyzmq`

19 | - `msgpack_python`

20 | - `python-snappy`

21 |

22 | 可以通过单个安装完成,例如: `pip install pyzmq`

23 |

24 | 需要注意的是,`python-snappy`的安装需要比较多的编译依赖,请按照[如何安装python-snappy包](https://github.com/quantOS-org/JAQS/blob/master/doc/install.md#如何安装python-snappy包)所述安装。

25 |

26 |

27 | ## 3、使用TradeApi

28 |

29 | 在项目目录,验证`TradeApi`是否能够正常使用。

30 |

31 | ```python

32 | from TradeApi import TradeApi # 这里假设项目目录名为TradeApi, 且存放在工作目录下

33 |

34 | api = TradeApi(addr="tcp://gw.quantos.org:8901")

35 | result, msg = api.login("username", "token") # 示例账户,用户需要改为自己在www.quantos.org上注册的账户

36 | print result

37 | print msg

38 | ```

39 |

--------------------------------------------------------------------------------

/doc/source/md2rst.py:

--------------------------------------------------------------------------------

1 | # encoding: utf-8

2 |

3 | import os

4 | from os.path import join

5 | import jaqs.util as jutil

6 | import subprocess

7 |

8 |

9 | def md2rst():

10 | input_dir = '..'

11 | output_dir = '.'

12 |

13 | for dir_path, dir_names, file_names in os.walk(input_dir):

14 | for fn in file_names:

15 | if fn.endswith('.md'):

16 | print("Converting {:s}...".format(fn))

17 |

18 | fn_pure = fn[:-2]

19 | fn_md = join(input_dir, fn)

20 | fn_html = join(input_dir, fn_pure+'html')

21 | fn_rst = join(output_dir, fn_pure+'rst')

22 |

23 | subprocess.check_output(['pandoc', fn_md,

24 | '-f', 'markdown_github',

25 | '-t', 'html', '-s', '-o', fn_html])

26 | subprocess.check_output(['pandoc', fn_html,

27 | '-f', 'html',

28 | '-t', 'rst', '-s', '-o', fn_rst])

29 | os.remove(fn_html)

30 |

31 |

32 | if __name__ == "__main__":

33 | md2rst()

--------------------------------------------------------------------------------

/jaqs/trade/event/eventtype.py:

--------------------------------------------------------------------------------

1 | # encoding: UTF-8

2 |

3 | from jaqs.trade import common

4 |

5 | '''

6 | 本文件仅用于存放对于事件类型常量的定义。

7 |

8 | 由于python中不存在真正的常量概念,因此选择使用全大写的变量名来代替常量。

9 | 这里设计的命名规则以EVENT_前缀开头。

10 |

11 | 常量的内容通常选择一个能够代表真实意义的字符串(便于理解)。

12 |

13 | 建议将所有的常量定义放在该文件中,便于检查是否存在重复的现象。

14 | '''

15 |

16 |

17 | class EVENT_TYPE(common.ReprStrEnum):

18 | TIMER = 'timer' # 计时器事件,每隔1秒发送一次

19 | MARKET_DATA = 'market_data' # 行情事件

20 |

21 | ORDER_RSP = 'order_rsp'

22 | TASK_RSP = 'task_rsp'

23 | TASK_STATUS_IND = 'task_callback'

24 | TRADE_IND = 'trade_ind' # 成交回报

25 | ORDER_STATUS_IND = 'order_status_ind' # 状态回报

26 |

27 | PLACE_ORDER = 'place_order'

28 | CANCEL_ORDER = 'cancel_order'

29 |

30 | QUERY_ACCOUNT = 'query_account'

31 | QUERY_UNIVERSE = 'query_universe'

32 | QUERY_PORTFOLIO = 'query_portfolio'

33 | QUERY_POSITION = 'query_position'

34 | QUERY_ORDER = 'query_order'

35 | QUERY_TASK = 'query_task'

36 | QUERY_TRADE = 'query_trade'

37 |

38 | GOAL_PORTFOLIO = 'goal_portfolio'

39 | STOP_PORTFOLIO = 'stop_portfolio'

40 |

41 | TRADE_API_DISCONNECTED = 'trade_api_disconnected'

42 | TRADE_API_CONNECTED = 'trade_api_connected'

43 |

--------------------------------------------------------------------------------

/doc/source/jaqs.data.basic.rst:

--------------------------------------------------------------------------------

1 | jaqs\.data\.basic package

2 | =========================

3 |

4 | Submodules

5 | ----------

6 |

7 | jaqs\.data\.basic\.instrument module

8 | ------------------------------------

9 |

10 | .. automodule:: jaqs.data.basic.instrument

11 | :members:

12 | :undoc-members:

13 | :show-inheritance:

14 |

15 | jaqs\.data\.basic\.marketdata module

16 | ------------------------------------

17 |

18 | .. automodule:: jaqs.data.basic.marketdata

19 | :members:

20 | :undoc-members:

21 | :show-inheritance:

22 |

23 | jaqs\.data\.basic\.order module

24 | -------------------------------

25 |

26 | .. automodule:: jaqs.data.basic.order

27 | :members:

28 | :undoc-members:

29 | :show-inheritance:

30 |

31 | jaqs\.data\.basic\.position module

32 | ----------------------------------

33 |

34 | .. automodule:: jaqs.data.basic.position

35 | :members:

36 | :undoc-members:

37 | :show-inheritance:

38 |

39 | jaqs\.data\.basic\.trade module

40 | -------------------------------

41 |

42 | .. automodule:: jaqs.data.basic.trade

43 | :members:

44 | :undoc-members:

45 | :show-inheritance:

46 |

47 |

48 | Module contents

49 | ---------------

50 |

51 | .. automodule:: jaqs.data.basic

52 | :members:

53 | :undoc-members:

54 | :show-inheritance:

55 |

--------------------------------------------------------------------------------

/doc/source/jaqs.util.rst:

--------------------------------------------------------------------------------

1 | jaqs\.util package

2 | ==================

3 |

4 | Submodules

5 | ----------

6 |

7 | jaqs\.util\.dtutil module

8 | -------------------------

9 |

10 | .. automodule:: jaqs.util.dtutil

11 | :members:

12 | :undoc-members:

13 | :show-inheritance:

14 |

15 | jaqs\.util\.fileio module

16 | -------------------------

17 |

18 | .. automodule:: jaqs.util.fileio

19 | :members:

20 | :undoc-members:

21 | :show-inheritance:

22 |

23 | jaqs\.util\.numeric module

24 | --------------------------

25 |

26 | .. automodule:: jaqs.util.numeric

27 | :members:

28 | :undoc-members:

29 | :show-inheritance:

30 |

31 | jaqs\.util\.pdutil module

32 | -------------------------

33 |

34 | .. automodule:: jaqs.util.pdutil

35 | :members:

36 | :undoc-members:

37 | :show-inheritance:

38 |

39 | jaqs\.util\.profile module

40 | --------------------------

41 |

42 | .. automodule:: jaqs.util.profile

43 | :members:

44 | :undoc-members:

45 | :show-inheritance:

46 |

47 | jaqs\.util\.sequence module

48 | ---------------------------

49 |

50 | .. automodule:: jaqs.util.sequence

51 | :members:

52 | :undoc-members:

53 | :show-inheritance:

54 |

55 |

56 | Module contents

57 | ---------------

58 |

59 | .. automodule:: jaqs.util

60 | :members:

61 | :undoc-members:

62 | :show-inheritance:

63 |

--------------------------------------------------------------------------------

/doc/source/jaqs.data.rst:

--------------------------------------------------------------------------------

1 | jaqs\.data package

2 | ==================

3 |

4 | Subpackages

5 | -----------

6 |

7 | .. toctree::

8 |

9 | jaqs.data.basic

10 | jaqs.data.dataapi

11 |

12 | Submodules

13 | ----------

14 |

15 | jaqs\.data\.align module

16 | ------------------------

17 |

18 | .. automodule:: jaqs.data.align

19 | :members:

20 | :undoc-members:

21 | :show-inheritance:

22 |

23 | jaqs\.data\.continueContract module

24 | -----------------------------------

25 |

26 | .. automodule:: jaqs.data.continueContract

27 | :members:

28 | :undoc-members:

29 | :show-inheritance:

30 |

31 | jaqs\.data\.dataservice module

32 | ------------------------------

33 |

34 | .. automodule:: jaqs.data.dataservice

35 | :members:

36 | :undoc-members:

37 | :show-inheritance:

38 |

39 | jaqs\.data\.dataview module

40 | ---------------------------

41 |

42 | .. automodule:: jaqs.data.dataview

43 | :members:

44 | :undoc-members:

45 | :show-inheritance:

46 |

47 | jaqs\.data\.py\_expression\_eval module

48 | ---------------------------------------

49 |

50 | .. automodule:: jaqs.data.py_expression_eval

51 | :members:

52 | :undoc-members:

53 | :show-inheritance:

54 |

55 |

56 | Module contents

57 | ---------------

58 |

59 | .. automodule:: jaqs.data

60 | :members:

61 | :undoc-members:

62 | :show-inheritance:

63 |

--------------------------------------------------------------------------------

/test/test_data_api.py:

--------------------------------------------------------------------------------

1 | # encoding: UTF-8

2 |

3 | from __future__ import print_function

4 | from jaqs.data import DataApi

5 | from jaqs.trade import common

6 | import jaqs.util as jutil

7 |

8 | from config_path import DATA_CONFIG_PATH

9 | data_config = jutil.read_json(DATA_CONFIG_PATH)

10 |

11 |

12 | def test_data_api():

13 | address = data_config.get("remote.data.address", None)

14 | username = data_config.get("remote.data.username", None)

15 | password = data_config.get("remote.data.password", None)

16 | if address is None or username is None or password is None:

17 | raise ValueError("no data service config available!")

18 |

19 | api = DataApi(address, use_jrpc=False)

20 | login_msg = api.login(username=username, password=password)

21 | print(login_msg)

22 |

23 | daily, msg = api.daily(symbol="600030.SH,000002.SZ", start_date=20170103, end_date=20170708,

24 | fields="open,high,low,close,volume,last,trade_date,settle")

25 | daily2, msg2 = api.daily(symbol="600030.SH", start_date=20170103, end_date=20170708,

26 | fields="open,high,low,close,volume,last,trade_date,settle")

27 | # err_code, err_msg = msg.split(',')

28 | assert msg == '0,'

29 | assert msg2 == '0,'

30 | assert daily.shape == (248, 9)

31 | assert daily2.shape == (124, 9)

32 |

33 | df, msg = api.bar(symbol="600030.SH", trade_date=20170904, freq=common.QUOTE_TYPE.MIN, start_time=90000, end_time=150000)

34 | print(df.columns)

35 | assert df.shape == (240, 15)

36 |

37 | print("test passed")

38 |

39 |

40 | if __name__ == "__main__":

41 | test_data_api()

42 |

--------------------------------------------------------------------------------

/jaqs/data/dataapi/.gitignore:

--------------------------------------------------------------------------------

1 | # Byte-compiled / optimized / DLL files

2 | __pycache__/

3 | *.py[cod]

4 | *$py.class

5 |

6 | # C extensions

7 | *.so

8 |

9 | # Distribution / packaging

10 | .Python

11 | env/

12 | build/

13 | develop-eggs/

14 | dist/

15 | downloads/

16 | eggs/

17 | .eggs/

18 | lib/

19 | lib64/

20 | parts/

21 | sdist/

22 | var/

23 | wheels/

24 | *.egg-info/

25 | .installed.cfg

26 | *.egg

27 |

28 | # PyInstaller

29 | # Usually these files are written by a python script from a template

30 | # before PyInstaller builds the exe, so as to inject date/other infos into it.

31 | *.manifest

32 | *.spec

33 |

34 | # Installer logs

35 | pip-log.txt

36 | pip-delete-this-directory.txt

37 |

38 | # Unit test / coverage reports

39 | htmlcov/

40 | .tox/

41 | .coverage

42 | .coverage.*

43 | .cache

44 | nosetests.xml

45 | coverage.xml

46 | *.cover

47 | .hypothesis/

48 |

49 | # Translations

50 | *.mo

51 | *.pot

52 |

53 | # Django stuff:

54 | *.log

55 | local_settings.py

56 |

57 | # Flask stuff:

58 | instance/

59 | .webassets-cache

60 |

61 | # Scrapy stuff:

62 | .scrapy

63 |

64 | # Sphinx documentation

65 | docs/_build/

66 |

67 | # PyBuilder

68 | target/

69 |

70 | # Jupyter Notebook

71 | .ipynb_checkpoints

72 |

73 | # pyenv

74 | .python-version

75 |

76 | # celery beat schedule file

77 | celerybeat-schedule

78 |

79 | # SageMath parsed files

80 | *.sage.py

81 |

82 | # dotenv

83 | .env

84 |

85 | # virtualenv

86 | .venv

87 | venv/

88 | ENV/

89 |

90 | # Spyder project settings

91 | .spyderproject

92 | .spyproject

93 |

94 | # Rope project settings

95 | .ropeproject

96 |

97 | # mkdocs documentation

98 | /site

99 |

100 | # mypy

101 | .mypy_cache/

102 |

--------------------------------------------------------------------------------

/jaqs/trade/tradeapi/.gitignore:

--------------------------------------------------------------------------------

1 | # Byte-compiled / optimized / DLL files

2 | __pycache__/

3 | *.py[cod]

4 | *$py.class

5 |

6 | # C extensions

7 | *.so

8 |

9 | # Distribution / packaging

10 | .Python

11 | env/

12 | build/

13 | develop-eggs/

14 | dist/

15 | downloads/

16 | eggs/

17 | .eggs/

18 | lib/

19 | lib64/

20 | parts/

21 | sdist/

22 | var/

23 | wheels/

24 | *.egg-info/

25 | .installed.cfg

26 | *.egg

27 |

28 | # PyInstaller

29 | # Usually these files are written by a python script from a template

30 | # before PyInstaller builds the exe, so as to inject date/other infos into it.

31 | *.manifest

32 | *.spec

33 |

34 | # Installer logs

35 | pip-log.txt

36 | pip-delete-this-directory.txt

37 |

38 | # Unit test / coverage reports

39 | htmlcov/

40 | .tox/

41 | .coverage

42 | .coverage.*

43 | .cache

44 | nosetests.xml

45 | coverage.xml

46 | *.cover

47 | .hypothesis/

48 |

49 | # Translations

50 | *.mo

51 | *.pot

52 |

53 | # Django stuff:

54 | *.log

55 | local_settings.py

56 |

57 | # Flask stuff:

58 | instance/

59 | .webassets-cache

60 |

61 | # Scrapy stuff:

62 | .scrapy

63 |

64 | # Sphinx documentation

65 | docs/_build/

66 |

67 | # PyBuilder

68 | target/

69 |

70 | # Jupyter Notebook

71 | .ipynb_checkpoints

72 |

73 | # pyenv

74 | .python-version

75 |

76 | # celery beat schedule file

77 | celerybeat-schedule

78 |

79 | # SageMath parsed files

80 | *.sage.py

81 |

82 | # dotenv

83 | .env

84 |

85 | # virtualenv

86 | .venv

87 | venv/

88 | ENV/

89 |

90 | # Spyder project settings

91 | .spyderproject

92 | .spyproject

93 |

94 | # Rope project settings

95 | .ropeproject

96 |

97 | # mkdocs documentation

98 | /site

99 |

100 | # mypy

101 | .mypy_cache/

102 |

--------------------------------------------------------------------------------

/doc/source/jaqs.trade.rst:

--------------------------------------------------------------------------------

1 | jaqs\.trade package

2 | ===================

3 |

4 | Subpackages

5 | -----------

6 |

7 | .. toctree::

8 |

9 | jaqs.trade.analyze

10 | jaqs.trade.event

11 | jaqs.trade.tradeapi

12 |

13 | Submodules

14 | ----------

15 |

16 | jaqs\.trade\.backtest module

17 | ----------------------------

18 |

19 | .. automodule:: jaqs.trade.backtest

20 | :members:

21 | :undoc-members:

22 | :show-inheritance:

23 |

24 | jaqs\.trade\.common module

25 | --------------------------

26 |

27 | .. automodule:: jaqs.trade.common

28 | :members:

29 | :undoc-members:

30 | :show-inheritance:

31 |

32 | jaqs\.trade\.livetrade module

33 | -----------------------------

34 |

35 | .. automodule:: jaqs.trade.livetrade

36 | :members:

37 | :undoc-members:

38 | :show-inheritance:

39 |

40 | jaqs\.trade\.model module

41 | -------------------------

42 |

43 | .. automodule:: jaqs.trade.model

44 | :members:

45 | :undoc-members:

46 | :show-inheritance:

47 |

48 | jaqs\.trade\.portfoliomanager module

49 | ------------------------------------

50 |

51 | .. automodule:: jaqs.trade.portfoliomanager

52 | :members:

53 | :undoc-members:

54 | :show-inheritance:

55 |

56 | jaqs\.trade\.strategy module

57 | ----------------------------

58 |

59 | .. automodule:: jaqs.trade.strategy

60 | :members:

61 | :undoc-members:

62 | :show-inheritance:

63 |

64 | jaqs\.trade\.tradegateway module

65 | --------------------------------

66 |

67 | .. automodule:: jaqs.trade.tradegateway

68 | :members:

69 | :undoc-members:

70 | :show-inheritance:

71 |

72 |

73 | Module contents

74 | ---------------

75 |

76 | .. automodule:: jaqs.trade

77 | :members:

78 | :undoc-members:

79 | :show-inheritance:

80 |

--------------------------------------------------------------------------------

/doc/base_data.md:

--------------------------------------------------------------------------------

1 | # 基础数据

2 |

3 |

4 | ## 调用说明

5 | - 通过api.query函数调用,第一个参数view需填入对应的接口名,如:`view="jz.instrumentInfo"`

6 | - 输入参数指的是filter参数里面的内容,通过'&'符号拼接,如:`filter="inst_type=&status=1&symbol="`

7 | - 输出参数指的是fields里面的内容,通过','隔开

8 |

9 | 样例代码:获取上市股票列表

10 | ```python

11 | df, msg = api.query(

12 | view="jz.instrumentInfo",

13 | fields="status,list_date, fullname_en, market",

14 | filter="inst_type=1&status=1&symbol=",

15 | data_format='pandas')

16 | ```

17 |

18 | ## 目前支持的接口及其含义

19 |

20 | | 接口 | view | 分类 |

21 | | ------------------ | --------------------- | ---------- |

22 | | 证券基础信息表 | jz.instrumentInfo | 基础信息 |

23 | | 交易日历表 | jz.secTradeCal | 基础信息 |

24 | | 分配除权信息表 | lb.secDividend | 股票 |

25 | | 复权因子表 | lb.secAdjFactor | 股票 |

26 | | 停复牌信息表 | lb.secSusp | 股票 |

27 | | 行业分类表 | lb.secIndustry | 股票 |

28 | | 日行情估值表 | lb.secDailyIndicator | 股票 |

29 | | 资产负债表 | lb.balanceSheet | 股票 |

30 | | 利润表 | lb.income | 股票 |

31 | | 现金流量表 | lb.cashFlow | 股票 |

32 | | 业绩快报 | lb.profitExpress | 股票 |

33 | | 限售股解禁表 | lb.secRestricted | 股票 |

34 | | 指数基本信息表 | lb.indexInfo | 指数 |

35 | | 指数成份股表 | lb.indexCons | 指数 |

36 | | 公募基金净值表 | lb.mfNav | 基金 |

37 | | 公募基金分红表 | lb.mfDividend | 基金 |

38 | | 公募基金股票组合表 | lb.mfPortfolio | 基金 |

39 | | 公募基金债券组合表 | lb.mfBondPortfolio | 基金 |

40 |

41 | 接口还在进一步的丰富过程中。

42 |

43 | 详细的说明文档,please refer to [quantos](https://www.quantos.org)

44 |

--------------------------------------------------------------------------------

/jaqs/util/numeric.py:

--------------------------------------------------------------------------------

1 | # encoding: utf-8

2 | import numpy as np

3 | import pandas as pd

4 |

5 |

6 | def quantilize_without_nan(mat, n_quantiles=5, axis=-1):

7 | mask = pd.isnull(mat)

8 | res = mat.copy()

9 |

10 | rank = res.argsort(axis=axis).argsort(axis=axis)

11 | count = np.sum(~mask, axis=axis) # int

12 |

13 | divisor = count * 1. / n_quantiles # float

14 | shape = list(res.shape)

15 | shape[axis] = 1

16 | divisor = divisor.reshape(*shape)

17 | res = np.floor(rank / divisor) + 1.0

18 |

19 | res[mask] = np.nan

20 |

21 | return res

22 |

23 | # res[~mask] = pd.qcut(mat[~mask], n_quantiles, labels = False) + 1

24 | # rank = mat.argsort(axis=axis).argsort(axis=axis) # int

25 | #

26 | # count = np.sum(~mask, axis=axis) # int

27 | # divisor = count * 1. / n_quantiles # float

28 | # shape = list(mat.shape)

29 | # shape[axis] = 1

30 | # divisor = divisor.reshape(*shape)

31 | #

32 | # res = np.floor(rank / divisor) + 1.0

33 | # res[mask] = np.nan

34 |

35 | #return res

36 |

37 |

38 | # Boolean, unsigned integer, signed integer, float, complex.

39 | _NUMERIC_KINDS = set('buifc')

40 |

41 |

42 | def is_numeric(array):

43 | """

44 | Determine whether the argument has a numeric datatype, when

45 | converted to a NumPy array.

46 |

47 | Booleans, unsigned integers, signed integers, floats and complex

48 | numbers are the kinds of numeric datatype.

49 |

50 | Parameters

51 | ----------

52 | array : array-like

53 | The array to check.

54 |

55 | Returns

56 | -------

57 | is_numeric : `bool`

58 | True if the array has a numeric datatype, False if not.

59 |

60 | """

61 | return np.asarray(array).dtype.kind in _NUMERIC_KINDS

62 |

--------------------------------------------------------------------------------

/doc/how_to_ask_questions.md:

--------------------------------------------------------------------------------

1 | # 如何正确提问

2 |

3 | 感谢大家的使用和建议,我们会持续改进。为了更高效地解决问题,请在提问时遵循一定的规范。

4 |

5 | ## 总结

6 |

7 | 附上代码、附上报错信息、附上Python版本和系统信息。

8 |

9 | ## 提问模板

10 |

11 | ```

12 | What steps will reproduce the problem?

13 | 该问题的重现步骤是什么?

14 | 1.

15 | 2.

16 | 3.

17 |

18 | What is the expected output? What do you see instead?

19 | 你期待的结果是什么?实际看到的又是什么?

20 |

21 |

22 | What version of the product are you using? On what operating system?

23 | 你正在使用产品的哪个版本?在什么操作系统上?

24 |

25 | Please provide any additional information below.

26 | 如果有的话,请在下面提供更多信息。

27 | ```

28 |

29 | ## 具体解释

30 |

31 | 什么是“最短代码-错误重现”提问方式?

32 |

33 | ### 帖子标题 = 帖子内容的提炼

34 |

35 | 简洁清晰,言之有物。让他人看了标题就能大概知道是否能帮助你,切勿使用“求助、急、帮忙、新手、高手、在线等”等无任何意义的词语。

36 |

37 | > 我遇到了一个 DataView的问题

38 | > TradeApi 在我的系统上运行不了

39 |

40 | 上面的标题很糟糕,光看标题作者无法知道发生了什么事。当开源社区的问题很多时,上面这类标题,经常会让作者直接忽视或将优先级降到很低。更妥当的标题是

41 |

42 | > DataView 在prepare_data时报NotLoginError

43 | > TradeApi 在 Ubuntu 14.04 上运行时提示-1,no connection

44 |

45 | ### 帖子正文 = 场景描述 + 代码 + 报错信息

46 |

47 | - 粘贴一个简单的程序程序代码

48 | - 贴出你的错误或警告信息(特别重要),以及你已经尝试过的方法、步骤(必要的时候,可以上传一些截图);

49 | - 写上你使用的是哪个MATLAB版本(如:64位R2012a等),以及操作系统(如:32位XP系统、64位Windows 7系统等)。

50 |

51 | #### 描述事实、而不是猜测

52 |

53 | 事实是指,依次进行了哪些操作、产生了怎样的结果。比如

54 |

55 | > 我在 Windows 10 下用 pip 打开JAQS后报错no snappy,按照安装指南安装python-snappy后,pandas包无法使用。

56 |

57 | 上面是一段比较好的事实描述(更好的是把错误提示也截图上来),而不要像下面这样猜测:

58 |

59 | > 安装JAQS导致pandas报错,我怀疑项目对Win10的兼容不好。

60 |

61 | 上面的描述,会让作者一头雾水。尽量避免猜测性描述,除非你能先描述事实,在事实描述清楚之后,再给出合理的猜测是欢迎的。

62 |

63 | #### 描述目标、而不是过程

64 |

65 | 经常会有这种情况,提问者在脑袋里有个更高层次的目标,他们在自以为能达到目标的特定道路上卡住了,然后跑来问该怎么走。举一个生活中的例子

66 |

67 | > 咖啡馆应该为每种咖啡提供5档不同甜度的版本

68 |

69 | 上面这个问题的背后,提问者认为不同顾客对甜度有不同偏好,咖啡馆在做咖啡时应满足。但事实上,正确的方式是提供糖,让顾客自己选择加多少。如果只是描述过程(提供不同甜度的咖啡)不描述目的(满足人们的甜度偏好),往往会把其他人也绕进去。

70 |

71 | 即很多情况下,对于要解决的问题,实际上有更好的方式。这种情况下,描述清楚目标,讲清楚要干什么非常重要。

72 |

73 |

74 |

75 | 本文参考了:[如何向开源社区提问题](https://github.com/seajs/seajs/issues/545)

76 |

--------------------------------------------------------------------------------

/.gitignore:

--------------------------------------------------------------------------------

1 | # Private files

2 | example/private/

3 |

4 | # cProfile results

5 | *.prof

6 |

7 | # Personal Configs

8 | # etc/*.json

9 |

10 | # IDE configs

11 | .idea/

12 | .eclipse/

13 |

14 | # Output Results

15 | output/

16 |

17 | # Byte-compiled / optimized / DLL files

18 | __pycache__/

19 | *.py[cod]

20 | *$py.class

21 |

22 | # C extensions

23 | *.so

24 |

25 | # Distribution / packaging

26 | .Python

27 | build/

28 | develop-eggs/

29 | dist/

30 | downloads/

31 | eggs/

32 | .eggs/

33 | lib/

34 | lib64/

35 | parts/

36 | sdist/

37 | var/

38 | wheels/

39 | *.egg-info/

40 | .installed.cfg

41 | *.egg

42 |

43 | # PyInstaller

44 | # Usually these files are written by a python script from a template

45 | # before PyInstaller builds the exe, so as to inject date/other infos into it.

46 | *.manifest

47 | *.spec

48 |

49 | # Installer logs

50 | pip-log.txt

51 | pip-delete-this-directory.txt

52 |

53 | # Unit test / coverage reports

54 | htmlcov/

55 | .tox/

56 | .coverage

57 | .coverage.*

58 | .cache

59 | nosetests.xml

60 | coverage.xml

61 | *.cover

62 | .hypothesis/

63 |

64 | # Translations

65 | *.mo

66 | *.pot

67 |

68 | # Django stuff:

69 | *.log

70 | local_settings.py

71 |

72 | # Flask stuff:

73 | instance/

74 | .webassets-cache

75 |

76 | # Scrapy stuff:

77 | .scrapy

78 |

79 | # Sphinx documentation

80 | docs/_build/

81 |

82 | # PyBuilder

83 | target/

84 |

85 | # Jupyter Notebook

86 | .ipynb_checkpoints

87 |

88 | # pyenv

89 | .python-version

90 |

91 | # celery beat schedule file

92 | celerybeat-schedule

93 |

94 | # SageMath parsed files

95 | *.sage.py

96 |

97 | # Environments

98 | .env

99 | .venv

100 | env/

101 | venv/

102 | ENV/

103 |

104 | # Spyder project settings

105 | .spyderproject

106 | .spyproject

107 |

108 | # Rope project settings

109 | .ropeproject

110 |

111 | # mkdocs documentation

112 | /site

113 |

114 | # mypy

115 | .mypy_cache/

116 |

117 | # output

118 | example/alpha/out/

119 | example/alpha/out2

120 |

--------------------------------------------------------------------------------

/setup.py:

--------------------------------------------------------------------------------

1 | from setuptools import setup, find_packages

2 | from jaqs import __version__ as ver

3 | import codecs

4 | import os

5 |

6 |

7 | def read(fname):

8 | return codecs.open(os.path.join(os.path.dirname(__file__), fname), 'r', encoding='utf-8').read()

9 |

10 |

11 | def readme():

12 | with codecs.open('README.rst', 'r', encoding='utf-8') as f:

13 | return f.read()

14 |

15 |

16 | def read_install_requires():

17 | with codecs.open('requirements.txt', 'r', encoding='utf-8') as f:

18 | res = f.readlines()

19 | res = list(map(lambda s: s.replace('\n', ''), res))

20 | return res

21 |

22 | setup(

23 | # Install data files specified in MANIFEST.in file.

24 | include_package_data=True,

25 | #package_data={'': ['*.json', '*.css', '*.html']},

26 | # Package Information

27 | name='jaqs',

28 | url='https://github.com/quantOS-org/JAQS',

29 | version=ver,

30 | license='Apache 2.0',

31 | # information

32 | description='Open source quantitative research&trading framework.',

33 | long_description=readme(),

34 | keywords="quantiatitive trading research finance",

35 | classifiers=[

36 | "Development Status :: 4 - Beta",

37 | "Intended Audience :: Developers",

38 | "Intended Audience :: Education",

39 | "Intended Audience :: End Users/Desktop",

40 | "Intended Audience :: Financial and Insurance Industry",

41 | "Intended Audience :: Information Technology",

42 | "Intended Audience :: Science/Research",

43 | "License :: OSI Approved :: Apache Software License",

44 | "Natural Language :: Chinese (Simplified)",

45 | "Natural Language :: English",

46 | "Operating System :: Microsoft :: Windows",

47 | "Operating System :: Unix",

48 | "Programming Language :: Python :: 2.7",

49 | "Programming Language :: Python :: 3.6",

50 | ],

51 | # install

52 | install_requires=read_install_requires(),

53 | packages=find_packages(),

54 | # author

55 | author='quantOS'

56 | )

57 |

--------------------------------------------------------------------------------

/doc/source/how_to_ask_questions.rst:

--------------------------------------------------------------------------------

1 | 如何正确提问

2 | ============

3 |

4 | 感谢大家的使用和建议,我们会持续改进。为了更高效地解决问题,请在提问时遵循一定的规范。

5 |

6 | 总结

7 | ----

8 |

9 | 附上代码、附上报错信息、附上Python版本和系统信息。

10 |

11 | 提问模板

12 | --------

13 |

14 | ::

15 |

16 | What steps will reproduce the problem?

17 | 该问题的重现步骤是什么?

18 | 1.

19 | 2.

20 | 3.

21 |

22 | What is the expected output? What do you see instead?

23 | 你期待的结果是什么?实际看到的又是什么?

24 |

25 |

26 | What version of the product are you using? On what operating system?

27 | 你正在使用产品的哪个版本?在什么操作系统上?

28 |

29 | Please provide any additional information below.

30 | 如果有的话,请在下面提供更多信息。

31 |

32 | 具体解释

33 | --------

34 |

35 | 什么是“最短代码-错误重现”提问方式?

36 |

37 | 帖子标题 = 帖子内容的提炼

38 | ~~~~~~~~~~~~~~~~~~~~~~~~~

39 |

40 | 简洁清晰,言之有物。让他人看了标题就能大概知道是否能帮助你,切勿使用“求助、急、帮忙、新手、高手、在线等”等无任何意义的词语。

41 |

42 | | 我遇到了一个 DataView的问题

43 | | TradeApi 在我的系统上运行不了

44 |

45 | 上面的标题很糟糕,光看标题作者无法知道发生了什么事。当开源社区的问题很多时,上面这类标题,经常会让作者直接忽视或将优先级降到很低。更妥当的标题是

46 |

47 | | DataView 在prepare\_data时报NotLoginError

48 | | TradeApi 在 Ubuntu 14.04 上运行时提示-1,no connection

49 |

50 | 帖子正文 = 场景描述 + 代码 + 报错信息

51 | ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

52 |

53 | - 粘贴一个简单的程序程序代码

54 | - 贴出你的错误或警告信息(特别重要),以及你已经尝试过的方法、步骤(必要的时候,可以上传一些截图);

55 | - 写上你使用的是哪个MATLAB版本(如:64位R2012a等),以及操作系统(如:32位XP系统、64位Windows

56 | 7系统等)。

57 |

58 | 描述事实、而不是猜测

59 | ^^^^^^^^^^^^^^^^^^^^

60 |

61 | 事实是指,依次进行了哪些操作、产生了怎样的结果。比如

62 |

63 | 我在 Windows 10 下用 pip 打开JAQS后报错no

64 | snappy,按照安装指南安装python-snappy后,pandas包无法使用。

65 |

66 | 上面是一段比较好的事实描述(更好的是把错误提示也截图上来),而不要像下面这样猜测:

67 |

68 | 安装JAQS导致pandas报错,我怀疑项目对Win10的兼容不好。

69 |

70 | 上面的描述,会让作者一头雾水。尽量避免猜测性描述,除非你能先描述事实,在事实描述清楚之后,再给出合理的猜测是欢迎的。

71 |

72 | 描述目标、而不是过程

73 | ^^^^^^^^^^^^^^^^^^^^

74 |

75 | 经常会有这种情况,提问者在脑袋里有个更高层次的目标,他们在自以为能达到目标的特定道路上卡住了,然后跑来问该怎么走。举一个生活中的例子

76 |

77 | 咖啡馆应该为每种咖啡提供5档不同甜度的版本

78 |

79 | 上面这个问题的背后,提问者认为不同顾客对甜度有不同偏好,咖啡馆在做咖啡时应满足。但事实上,正确的方式是提供糖,让顾客自己选择加多少。如果只是描述过程(提供不同甜度的咖啡)不描述目的(满足人们的甜度偏好),往往会把其他人也绕进去。

80 |

81 | 即很多情况下,对于要解决的问题,实际上有更好的方式。这种情况下,描述清楚目标,讲清楚要干什么非常重要。

82 |

83 | 本文参考了:\ `如何向开源社区提问题 `__

84 |

--------------------------------------------------------------------------------

/jaqs/trade/analyze/static/bootstrap-toc/bootstrap-toc.min.css:

--------------------------------------------------------------------------------

1 | /*!

2 | * Bootstrap Table of Contents v<%= version %> (http://afeld.github.io/bootstrap-toc/)

3 | * Copyright 2015 Aidan Feldman